Tether's "son" STABLE crashes? Plunges 60% on first day, whale front-running and no CEX listing spark trust panic

The Stable public blockchain has launched its mainnet. As a project associated with Tether, it has attracted significant attention but performed poorly in the market, with its price plummeting by 60% and facing a crisis of confidence. It is also confronted with fierce competition and challenges related to its tokenomics. Summary generated by Mars AI. The accuracy and completeness of the content are still being iteratively updated.

Another stablecoin bearing the title of “Tether’s protégé” has officially launched, but the market doesn’t seem to be buying it.

On the evening of December 8, the highly anticipated stablecoin-dedicated public chain Stable officially launched its mainnet and STABLE token. As a Layer 1 deeply incubated by the core teams of Bitfinex and Tether, the “Tether’s protégé” narrative attracted widespread attention from the market as soon as Stable debuted.

However, against the backdrop of tightening market liquidity, Stable did not have a strong start like its competitor Plasma. Not only did its price remain sluggish, but it also fell into a trust crisis due to allegations of insider trading. Is Stable’s script to first suppress and then rise, or will it continue to underperform?

STABLE drops 60% from launch high, mired in insider trading trust crisis

Before Stable’s launch, market sentiment was quite optimistic. The project’s two rounds of pre-deposits totaled over 1.3 billions USD, with about 25,000 participating addresses and an average deposit of approximately 52,000 USD per address, indicating strong user interest. This was rare during a period of market depression and showed high recognition of the “Tether-backed” endorsement, with hopes that STABLE’s debut could replay Plasma’s legendary wealth creation.

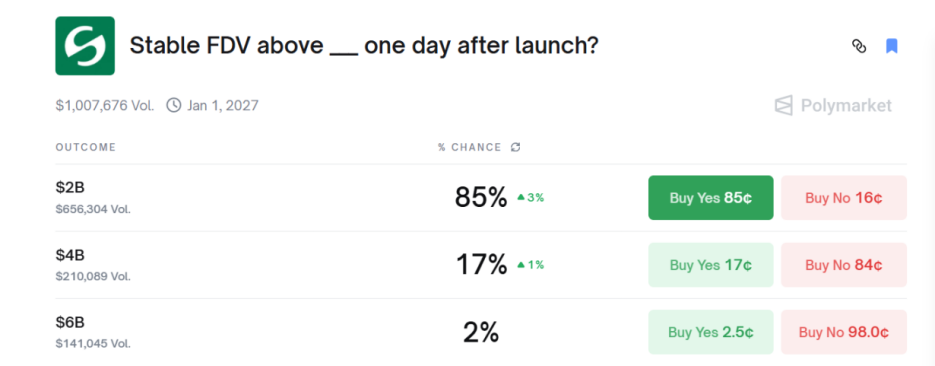

According to prediction market Polymarket, there was once an 85% probability that STABLE’s FDV (fully diluted valuation) would exceed 2 billions USD.

However, the “hot must die” rule proved true once again.

STABLE’s performance on its TGE (Token Generation Event) day was disappointing. The opening price was about $0.036, with a post-launch high near $0.046, then it dropped over 60%, hitting a low of $0.015. As of 9:00 PM on December 9, STABLE’s FDV had shrunk to $1.7 billions, and with thin liquidity, no one in the market was willing to buy in.

It’s worth noting that leading CEXs (centralized exchanges) such as Binance, Coinbase, and Upbit have not yet listed the STABLE token on their spot markets. Their absence has limited STABLE’s reach to a broader retail audience, further restricting its liquidity.

The sharp drop in STABLE’s price also sparked heated discussions in the community.

DeFi researcher @cmdefi commented: Expectations for Stable are relatively low, and there were various amateurish operations during the early project launch, raising concerns about the team’s seriousness.

Crypto KOL @cryptocishanjia pointed out: The crowd is more willing to pay for new narratives. Once the market already has a leader (Plasma), consensus on the second (Stable) will greatly increase, thus reducing profit margins.

Former VC professional @Michael_Liu93 bluntly stated: The $3 billions pre-market plus an inflated FDV makes Stable a good long-term short target. Tight control (no airdrop, no presale, no KOL round) doesn’t mean price pumping, but since it hasn’t been listed on top CEXs, a reversal might occur.

Additionally, many users mentioned the controversy over pre-deposits before Stable’s mainnet launch. In the first round of pre-deposits, a whale wallet deposited hundreds of millions of USDT before the official deposit window opened, sparking strong suspicions of unfairness and insider trading within the community. The project team did not respond directly and proceeded to the second round of pre-deposits.

This event created a paradox in Stable’s narrative: its value proposition is to provide transparent, reliable, and compliant infrastructure. Yet, the project faced suspected insider trading at its inception, creating a trust deficit that could hinder community participation and negatively impact its long-term narrative.

USDT as Gas Fee Optimizes Payment Experience, Tokenomics Raise Concerns

Stable’s architecture is designed to maximize transaction efficiency and user-friendliness.

Stable is the first L1 to use USDT as the native gas fee, offering a near gasless user experience. The significance of this design is that it minimizes user friction. Users can pay transaction fees with the medium of exchange itself (USDT) without managing or holding highly volatile governance tokens. This feature enables sub-second settlement and minimal fees, especially suitable for daily transactions and institutional payments that require strict price stability and predictability.

Stable adopts the StableBFT consensus mechanism, a customized DPoS (Delegated Proof of Stake) model based on CometBFT (formerly Tendermint), and is fully EVM (Ethereum Virtual Machine) compatible. StableBFT uses Byzantine fault tolerance to guarantee transaction finality, meaning once a transaction is confirmed, it is irreversible—crucial for payment and settlement scenarios. In addition, StableBFT supports nodes processing proposals in parallel, ensuring the network achieves both high throughput and low latency to meet the demanding requirements of payment networks.

Stable secured strong capital backing from the outset. The project raised $28 millions in seed funding, led by Bitfinex and Hack VC. Paolo Ardoino, CEO of Tether/Bitfinex, serves as an advisor, leading the market to speculate about a close strategic synergy between Stable and stablecoin giant Tether.

Stable CEO Brian Mehler previously served as VP of Venture Capital at Block.one, the developer of EOS, managing a $1 billions crypto fund and investing in industry giants such as Galaxy Digital and Securitize.

The CTO is Sam Kazemian, founder of the hybrid algorithmic stablecoin project Frax, who has been deeply involved in DeFi for years and has advised on US stablecoin legislation.

However, Stable’s initial CEO was Joshua Harding, former head of investments at Block.one. The project changed leadership without any announcement or explanation, casting a shadow over Stable’s transparency.

Stable’s tokenomics adopt a strategy of separating network utility and governance value. The sole purpose of the STABLE token is governance and staking. It is not used to pay any network fees; all transactions are settled in USDT.

Token holders can stake STABLE to become validators and maintain network security. They can also participate in community voting on network upgrades, fee adjustments, or the introduction of new stablecoins. Since holders cannot share in network revenue, this weakens the token’s appeal, and before the ecosystem matures, the token lacks utility.

Notably, 50% of the total token supply (100 billions) will be allocated to the team, investors, and advisors. Although these tokens are subject to a one-year cliff before linear release, the significant allocation to insiders could exert long-term downward pressure on the token price.

Fierce Competition in the Stablecoin Public Chain Track, Execution Will Be the Deciding Factor

Stable faces extremely fierce market competition. In today’s multi-chain landscape, Polygon and Tron have a large retail user base for low-cost remittances in Southeast Asia, South America, the Middle East, and Africa, while Solana also occupies a place in the payments sector thanks to its high throughput performance.

More importantly, Stable also faces competition from emerging vertical L1s dedicated to stablecoin payments. For example, Circle’s Arc focuses on being institutional-grade on-chain treasury, global settlement, and tokenization infrastructure. Additionally, Tempo, backed by Stripe and Paradigm, is also positioned as a payment public chain and a strong competitor in the same vertical.

In the payments and settlement sector, network effects will be the core winning factor. Stable’s success will depend on whether it can quickly leverage the USDT ecosystem to attract developers and institutional users, and establish a first-mover advantage in large-scale settlement. If execution and market penetration are insufficient, it may be overtaken by similar L1s with stronger integration capabilities or deeper compliance backgrounds.

According to its roadmap, the main milestones are enterprise integration and developer ecosystem building in 2025 Q4 - 2026 Q2. Whether these goals can be achieved will be key to verifying Stable’s value proposition and the feasibility of a vertical L1. However, with only about six months from mainnet launch to pilot implementation, Stable must quickly overcome multiple challenges in technical optimization, institutional integration, and ecosystem cultivation. Any execution misstep could further erode market confidence in its long-term potential.

The launch of Stable’s mainnet marks a new phase of infrastructure-level competition in the stablecoin sector, and whether it can reshape payment networks will ultimately depend on execution, not narrative.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Tether: A "dangerous" asset swap worth billions of dollars?

Bitwise CIO: 2026 will be very strong; ICOs will make a comeback

Bitcoin’s back above $94K: Is the BTC bull run back on?