After bitcoin returns to $90,000, is Christmas or a Christmas crash coming next?

This Thanksgiving, we are grateful for bitcoin returning to $90,000.

No matter if you are Chinese or foreign, everyone shares the traditional mindset of “reuniting and celebrating festivals together.” The fourth Thursday of November each year is Thanksgiving, a major traditional holiday in the United States.

This year, the thing crypto people are most grateful for on Thanksgiving might be bitcoin returning to $90,000.

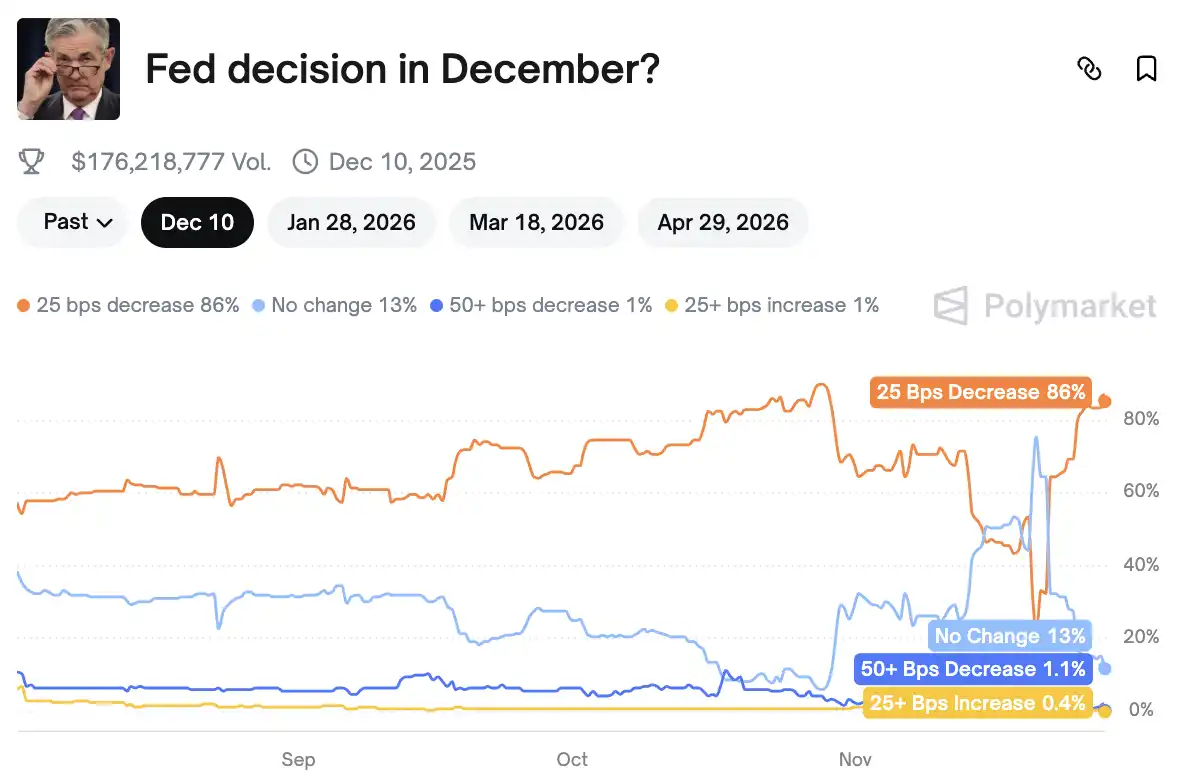

Aside from the influence of the “holiday market,” a “Beige Book” that unexpectedly became a key decision-making reference due to the government shutdown also helped rewrite the direction of this year’s final monetary policy. The probability of a Federal Reserve rate cut in December soared from 20% a week ago to 86%.

When the Federal Reserve’s stance reverses, when major global economies simultaneously start the “money printing mode,” and as cracks in the traditional financial system widen, crypto assets are standing before their most crucial seasonal window. Once the floodgates of global liquidity open, how will it affect the direction of the crypto industry? More importantly, is the upcoming holiday going to be a Christmas celebration or a Christmas disaster?

The Probability of a December Rate Cut Soars to 86%

According to Polymarket data, the probability of the Federal Reserve cutting rates by 25 basis points at its December meeting has soared from about 20% a week ago to 86%. This is likely one of the main reasons for bitcoin’s recent surge, and the reversal in probability is due to an economic report—the “Beige Book.”

An Important Report Deciding the Rate Cut

On Wednesday, the “Beige Book,” compiled by the Dallas Fed and summarizing the latest conditions from 12 regions across the U.S., was officially released. Normally, it’s just a routine document, but due to the government shutdown causing many key economic data releases to be delayed, this report instead became a rare and comprehensive information source that the FOMC could rely on before making decisions.

In other words, in the absence of data, this is one of the few windows through which the Federal Reserve can truly observe the grassroots economic situation.

The overall assessment given by the report is direct: economic activity has barely changed, labor demand continues to weaken, business cost pressures have increased, and consumers are becoming more cautious in their spending. Beneath the surface stability of the U.S. economy, some structural loosening is beginning to appear.

The most closely watched part of the report is its description of changes in the job market. Over the past six weeks, there have been few positive signs in the U.S. labor market. About half of the regional Feds reported that local businesses are less willing to hire, with some even showing a tendency to “avoid hiring if possible.” The difficulty of hiring has noticeably decreased across multiple industries, a stark contrast to the severe labor shortages of the past two years. For example, in the Atlanta district covering several southeastern states, many companies are either laying off workers or only minimally replacing those who leave; in the Cleveland district, which includes Ohio and Pennsylvania, some retailers are actively reducing staff due to declining sales. These changes mean that labor market loosening is no longer isolated but is gradually spreading to more industries and regions.

Meanwhile, although inflation pressure is described as “moderate,” the reality for businesses is more complicated than the numbers suggest. Some manufacturing and retail companies are still under pressure from rising input costs, with tariffs being one reason—for example, a brewery in the Minneapolis district reported that higher aluminum can prices have significantly increased production costs. But even more challenging are healthcare costs, which were mentioned by nearly all districts. Providing healthcare benefits for employees is becoming increasingly expensive, and unlike tariffs, these costs are not cyclical but represent a long-term trend that is harder to reverse. As a result, companies are forced to make tough choices between “raising prices” and “shrinking profits.” Some pass costs on to consumers, pushing prices higher; others absorb the costs themselves, further squeezing profit margins. Either way, the impact will eventually show up in CPI and corporate earnings in the coming months.

Compared to business-side pressures, changes on the consumer side are equally significant. High-income groups continue to support strong performance in high-end retail, but broader American households are tightening their spending. Several regions noted that consumers are increasingly resistant to price increases, especially middle- and low-income families, who are more likely to delay or forgo non-essential purchases when budgets are tight. Feedback from car dealers is especially telling: as federal tax subsidies expire, electric vehicle sales have slowed rapidly, indicating that consumers are becoming more cautious about large expenditures, even in previously booming sectors.

Among various economic disruptions, the impact of the government shutdown is clearly amplified in this report. The shutdown lasted a record length, directly affecting the incomes of federal employees, whose reduced spending also dragged down local consumption—Philadelphia district car sales dropped significantly as a result. But what’s truly surprising is that the shutdown affected broader economic activity through other channels. Some airports in the Midwest became chaotic due to fewer travelers, slowing down business activity as well. Some companies also experienced order delays. This chain reaction shows that the economic impact of a government shutdown goes far beyond the mere “suspension of government functions.”

On a more macro-technical level, artificial intelligence is quietly changing the economic structure. Respondents in the “Beige Book” presented a subtle “dual-track phenomenon”: on one hand, AI is driving investment growth, such as a Boston district manufacturer receiving more orders due to strong demand for AI infrastructure; on the other hand, some companies are cutting entry-level positions as basic tasks are partially replaced by AI tools. Even the education sector is seeing similar concerns—colleges in the Boston area report that many students worry traditional jobs will be affected by AI in the future, so they are more inclined to switch to “risk-resistant” fields like data science. This means AI’s restructuring of the economy has already penetrated from the industrial level to the talent supply side.

It’s worth noting that the changes presented in the “Beige Book” are corroborated by the latest data. Signs of labor market weakness are appearing simultaneously in multiple districts, while on the price side, the Producer Price Index (PPI) is up only 2.7% year-on-year, the lowest since July, and core prices are showing a continued softening trend with no signs of reigniting. These two indicators—employment and inflation—are directly related to monetary policy and are causing the market to reassess the Federal Reserve’s next move.

Economic “Fatigue” Spreads Across Regional Feds

National trends can be seen in macro data, but regional Fed reports are more like zooming in on businesses and households, making it clear that the U.S. economic slowdown is not uniform but shows a “distributed fatigue.”

In the Northeast, businesses in the Boston district generally reported slight expansion in economic activity, with home sales regaining some momentum after a long stagnation. But consumer spending merely held steady, employment declined slightly, and wage growth moderated. Rising food costs pushed up grocery prices, but overall price pressures remained manageable, and the outlook was cautiously optimistic.

The situation in the New York area is noticeably colder. There, economic activity declined moderately, many large employers began layoffs, and employment shrank slightly. Price increases slowed but remained high; manufacturing recovered slightly, but consumer spending continued to weaken, with only high-end retail remaining resilient. Business expectations for the future were generally low, with many believing the economy would not improve significantly in the short term.

Further south, the Philadelphia Fed described a reality where “weakness appeared even before the shutdown.” Most industries are experiencing moderate declines, employment is decreasing in tandem, and price pressures are squeezing the living space of middle- and low-income families, while recent policy changes have left many small and medium-sized businesses feeling cornered.

Further down, the Richmond district appears slightly more resilient. The overall economy maintained moderate growth, consumers hesitated over large purchases, but daily spending grew slowly. Manufacturing activity contracted slightly, while other industries were mostly flat. Employment showed no significant change, employers preferred to maintain existing team sizes, and both wages and prices were rising moderately.

The Atlanta Fed, covering the South, is more like a “standing still” state: economic activity is generally flat, employment is stable, and both prices and wages are rising moderately. Retail growth slowed, tourism dipped slightly, real estate remained under pressure, but commercial real estate showed some signs of stabilizing. Energy demand grew slightly, while manufacturing and transportation maintained low-speed operations.

In the central St. Louis district, overall economic activity and employment showed “no significant change,” but demand is further slowing due to the government shutdown. Prices are rising moderately, but businesses generally worry that increases will accelerate over the next six months. Under the dual pressure of economic slowdown and rising costs, local business confidence has become somewhat pessimistic.

Piecing together these local reports, we see the outline of the U.S. economy: no full-blown recession, no clear recovery, but a scattered display of varying degrees of fatigue. It is this set of “different temperatures” from local samples that forces the Federal Reserve to face a more realistic problem before its next meeting—the cost of high interest rates is fermenting in every corner.

Federal Reserve Officials Shift Their Tone

If the “Beige Book” clearly presents the “expression” of the real economy, then statements from Federal Reserve officials over the past two weeks further reveal a quiet policy shift at the top. Subtle changes in tone may seem like mere wording adjustments to outsiders, but at this stage, any change in tone often signals a shift in internal risk assessment.

Several heavyweight officials have begun to emphasize the same fact: the U.S. economy is cooling, prices are falling faster than expected, and the slowdown in the labor market is “worth watching.” Compared to their nearly unanimous stance over the past year of “maintaining a sufficiently tight policy environment,” the tone is now noticeably softer. Especially regarding employment, their statements have become particularly cautious, with some officials frequently using words like “stable,” “slowing,” and “moving toward a more balanced direction,” rather than emphasizing “still overheated.”

This kind of description rarely appears at the end of a hawkish cycle; it’s more like a tactful way of saying, “We’re seeing some early signs, and current policy may already be tight enough.”

Some officials have even explicitly mentioned that over-tightening policy could bring unnecessary economic risks. The appearance of this statement is itself a signal: when they start to guard against the side effects of “over-tightening,” it means policy direction is no longer one-way, but has entered a stage that requires fine-tuning and balance.

These changes have not escaped the market’s attention. Interest rate traders were the first to react, with futures market pricing showing significant jumps within days. Expectations for a rate cut, previously thought to be “no earlier than mid-next year,” have gradually moved up to spring. The “rate cut before mid-year,” which no one dared discuss publicly a few weeks ago, is now appearing in many investment banks’ baseline forecasts. The market logic is not complicated:

If employment continues to weaken, inflation continues to fall, and economic growth hovers near zero for a long time, maintaining excessively high interest rates will only make the problem worse. The Federal Reserve will ultimately have to choose between “sticking to tightening” and “preventing a hard landing,” and current signs suggest the balance is starting to tip.

Therefore, as the “Beige Book” depicts the economy cooling to “slightly chilly,” the Federal Reserve’s changing attitude and the market’s repricing are starting to reinforce each other. The same narrative logic is taking shape: the U.S. economy is not plummeting, but its momentum is slowly running out; inflation has not disappeared, but it is moving in a “controllable” direction; policy has not clearly shifted, but it is no longer in last year’s unhesitating tightening stance.

A New Cycle of Global Liquidity

The Anxiety Behind Japan’s 11.5 Trillion Yen in New Debt

While expectations are loosening in the U.S., major overseas economies are also quietly pushing the curtain up on “global reflation,” such as Japan.

The scale of Japan’s latest stimulus plan is much larger than outsiders imagine. On November 26, multiple media outlets cited sources saying that Prime Minister Sanae Takaichi’s government will issue at least 11.5 trillion yen (about $73.5 billion) in new bonds for the latest economic stimulus package. This is almost double the size of last year’s stimulus budget under Shigeru Ishiba. In other words, Japan’s fiscal direction has shifted from “cautious” to “must support the economy.”

Although authorities expect tax revenue to reach a record 80.7 trillion yen this fiscal year, the market is not reassured. Investors are more concerned about Japan’s long-term fiscal sustainability. This also explains why the yen has been continuously sold off recently, Japanese government bond yields have soared to a 20-year high, and the USD/JPY exchange rate remains elevated.

At the same time, this stimulus package is expected to boost actual GDP by 24 trillion yen, with an overall economic impact close to $26.5 billion.

Domestically, Japan is also trying to suppress short-term inflation with subsidies, such as a 7,000 yen utility subsidy per household for three consecutive months to stabilize consumer confidence. But the deeper impact is on capital flows—the continued weakening of the yen is prompting more and more Asian funds to consider new allocation directions, and crypto assets are right at the forefront of the risk curve they are willing to test.

Crypto analyst Ash Crypto has already discussed Japan’s “money printing” move alongside the Federal Reserve’s policy shift, believing it will push the risk appetite cycle all the way to 2026. And Dr. Jack Kruse, a long-time bitcoin supporter, interprets it more directly: high Japanese bond yields are themselves a signal of fiat system stress, and bitcoin is one of the few assets that can continually prove itself in such cycles.

Britain’s Debt Crisis Feels Like 2008 Again

Now let’s look at the UK, which has recently stirred up quite a storm.

If Japan is flooding the market, and China is stabilizing liquidity, then the UK’s fiscal operations at this moment look more like adding weight to an already leaking ship. The latest budget announcement has almost caused collective frowns in London’s financial circles.

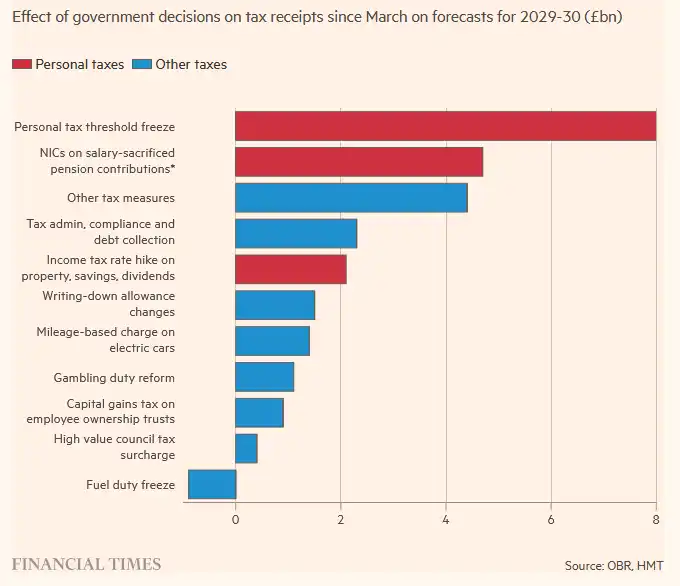

The Institute for Fiscal Studies, regarded as one of the most authoritative analytical institutions, gave an unequivocal assessment: “Spend now, pay later.” In other words, spending is rolled out immediately, but tax increases won’t take effect for several years—this is a standard “leave the problem for future governments” fiscal structure.

The most eye-catching part of the budget is the extension of the personal income tax threshold freeze. This seemingly minor technical move will contribute £12.7 billion to the Treasury in the 2030-31 fiscal year. According to the Office for Budget Responsibility, by the end of the budget cycle, a quarter of UK workers will be pushed into the 40% higher tax bracket. This means that even if Labour MPs cheer for higher landlord and dividend taxes, the real and sustained pressure will still fall on ordinary wage earners.

In addition, tax increases keep coming: tax relief for pension salary sacrifice schemes will be limited, expected to contribute nearly £5 billion by 2029-30; from 2028, properties worth over £2 million will be subject to an annual “mansion tax”; from 2026, dividend tax will rise by two percentage points, with the basic and higher rates jumping to 10.75% and 35.75%. All these seemingly “tax the rich” policies will ultimately be passed on to society in more subtle ways.

In exchange for higher taxes, welfare spending will expand immediately. According to OBR estimates, by 2029-30, annual welfare spending will be £16 billion more than previously forecast, including extra costs from overturning the “two-child benefit cap.” The contours of fiscal pressure are becoming clearer: short-term political gains, long-term fiscal black holes.

This year’s budget backlash is fiercer than in previous years, partly because the UK’s fiscal gap is no longer just “widening a bit,” but is approaching crisis levels. In the past seven months, the UK government has borrowed £117 billion, almost equal to the amount used to bail out the entire banking system during the 2008 financial crisis. In other words, the debt hole the UK is creating now is at crisis scale, even without a crisis.

Even the usually mild Financial Times has unusually used the word “brutal,” pointing out that the government still does not understand a basic issue: in a long-term stagnant economy, repeatedly raising tax rates to fill the gap is doomed to fail.

The market’s view of the UK has become extremely pessimistic: the UK “has no money,” and the ruling party seems to have no viable growth path, only pointing to higher taxes, weaker productivity, and higher unemployment. As the fiscal gap continues to widen, debt is likely to be “de facto monetized”—the ultimate pressure will fall on the pound, becoming the market’s “escape valve.”

This is also why more and more analysis is spreading from traditional finance to the crypto world, with some directly concluding: when currency starts to depreciate passively, and wage earners and the asset-less are slowly pushed to the edge, the only thing that cannot be arbitrarily diluted is hard assets—including bitcoin.

Christmas or Christmas Disaster?

At the end of each year, the market habitually asks: will this year be a “Christmas rally” or a “Christmas disaster”?

Thanksgiving is almost over, and its “seasonal benefit” for U.S. stocks has been discussed in the market for decades.

The difference this year is that the correlation between the crypto market and U.S. stocks is now close to 0.8, with price movements almost in sync. On-chain accumulation signals are strengthening, and the low liquidity during the holidays often amplifies any upward movement into a “vacuum rebound.”

The crypto community is also repeatedly emphasizing the same thing: holidays are the easiest windows for short-term trend moves. Low trading volume means lighter buying can push prices out of dense trading zones, especially when sentiment is currently cool and chips are more stable.

You can sense a quiet consensus forming in the market: if U.S. stocks start a small rebound after Black Friday, crypto will be the most reactive asset class; and Ethereum is seen by many institutions as “equivalent to a high-beta small-cap stock.”

Looking further ahead, shifting the focus from Thanksgiving to Christmas, the core discussion has changed from “will the market rise” to “will this seasonal rally continue into next year.”

The so-called “Santa Claus rally” was first proposed in 1972 by Yale Hirsch, founder of the Stock Trader’s Almanac, and gradually became one of the many seasonal effects in U.S. stocks. It refers to the last five trading days of December and the first two trading days of the following year, during which U.S. stocks usually see a rise.

The S&P index has closed higher around Christmas in 58 out of the past 73 years, with a win rate close to 80%.

More importantly, if a Santa Claus rally occurs, it may be a sign that the stock market will perform well the following year. According to Yale Hirsch’s analysis, if the Santa Claus rally, the first five trading days of the new year, and the January barometer are all positive, then the U.S. stock market is likely to perform well in the new year.

In other words, these few days at the end of the year are the most indicative micro-window of the entire year.

For bitcoin, the fourth quarter has historically been its easiest period to start a trend. Whether it’s the early miner cycles or later institutional allocation rhythms, Q4 has become a natural “right-side market season.” This year, it’s compounded by new variables: U.S. rate cut expectations, improved Asian liquidity, clearer regulation, and institutional position inflows.

So the question becomes a more practical judgment: if U.S. stocks enter a Santa Claus rally, will bitcoin go even higher? If U.S. stocks don’t rally, will bitcoin move on its own?

All of this will determine whether crypto industry participants are about to have a Christmas celebration or a Christmas disaster.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump vs JPMorgan: The Ultimate Showdown Between Two Dollar Monetary Orders and the New Era of Bitcoin

ETH traders ramp up positioning, setting a price target at $3.4K

BTC price pauses at $92K: Can Bitcoin avoid another crash?

Crypto bull market signal: ERC-20 stablecoin supply preserves $185B record