Triple Pressure on the Crypto Market: ETF Outflows, Leverage Reset, and Low Liquidity

In the recent cryptocurrency market downturn, the main factors include a slowdown in ETF inflows, deleveraging impacts, and liquidity constraints, placing the market in a fragile adjustment period amid macro risk-off sentiment.

Original Article Title: Crypto at the Crossroads: ETF Flows, Leverage Reset, and Shallow Liquidity

Original Article Author: Tanay Ved, Coin Metrics

Original Article Translation: Luffy, Foresight News

TL;TR

Major fund inflows channels such as ETFs and DAT have recently experienced weak demand, the October deleveraging process, and the macro hedging background continue to exert pressure on the cryptocurrency market. Futures and DeFi lending markets have completed a comprehensive leverage reset, with the ownership structure becoming cleaner and systemic risk somewhat reduced. The spot liquidity of both mainstream and altcoins has not yet recovered, and the market remains fragile, making it more prone to extreme price fluctuations.

Early in Uptober, Bitcoin briefly surged to a new all-time high, but the optimistic sentiment quickly reversed, with the "10.11" flash crash severely impacting market confidence (Note: Uptober refers to the cryptocurrency market usually experiencing an uptrend in October). Since then, the price of Bitcoin has dropped by about $40,000 (a drop of over 33%), while altcoins have suffered a greater impact, causing the total cryptocurrency market capitalization to fall to nearly $3 trillion. Despite several favorable fundamental developments throughout 2025, the price trend has significantly deviated from market sentiment.

Currently, cryptocurrencies are at a crossroads of multiple external and internal factors. At the macro level, the uncertainty surrounding the December rate cut expectations and the recent weakness in tech stocks have further intensified market risk aversion behavior. Internally in the crypto market, ETFs and Digital Asset Treasuries (DAT) that once served as stable fund inflow channels have experienced outflows; meanwhile, the "10.11" liquidation event triggered one of the most severe deleveraging events in history, with its ongoing effects still persisting, keeping market liquidity low.

This article will delve deep into the core driving factors behind the recent weakness in the cryptocurrency market, examining the ETF fund flows, leverage status in perpetual futures and DeFi markets, and order book liquidity, to explore the current market landscape revealed by these changes.

Macro Shift Towards Risk-Off Mode

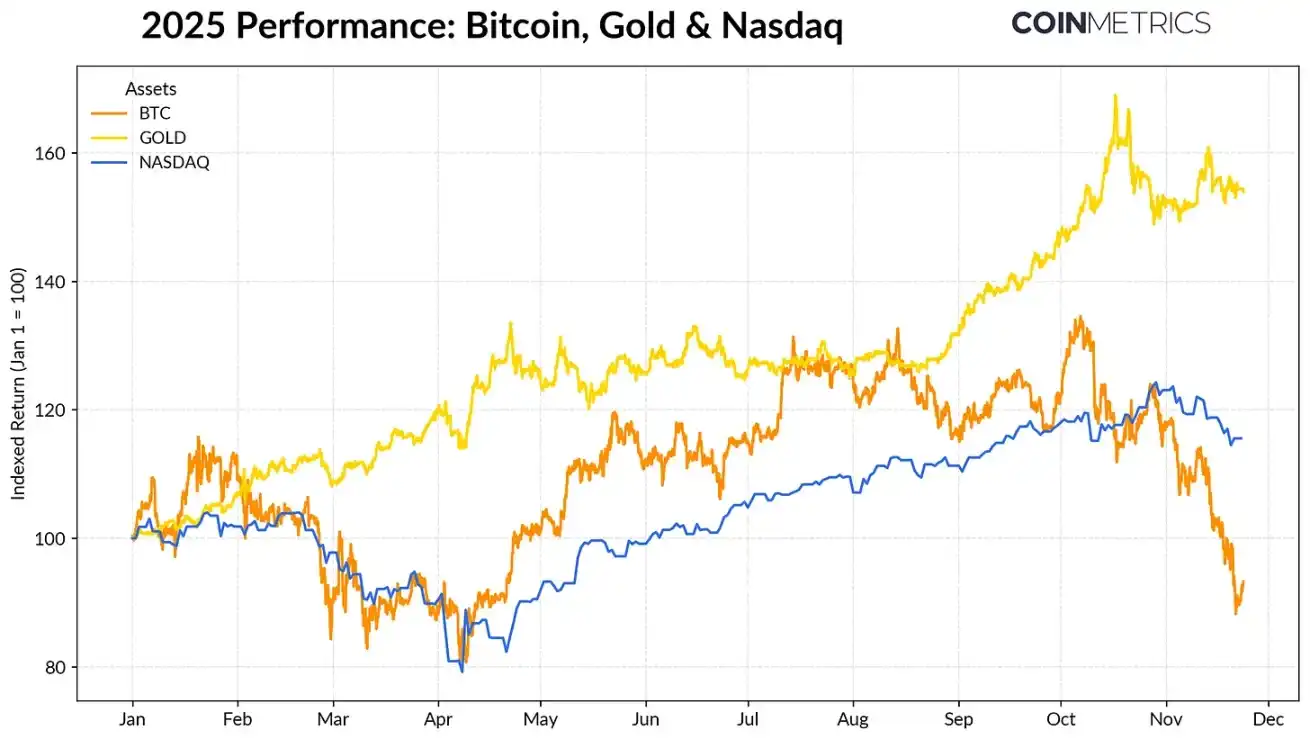

Bitcoin's performance has increasingly diverged from major asset classes. Against the backdrop of central banks' record purchases of gold and ongoing trade tensions, gold has delivered a return of over 50% this year, surging continuously, while tech stocks (Nasdaq index) lost momentum in the fourth quarter as the market reassesses the likelihood of an upcoming Fed rate cut and the sustainability of an AI-driven bull market.

As shown in our previous research, Bitcoin has exhibited cyclical relationships with "risk-on" tech stocks and "risk-off" gold, adjusting in response to macroeconomic trends. This makes Bitcoin particularly sensitive to market shocks or catalyst events (such as the October flash crash and recent risk-off sentiment).

In 2025, the performance of Bitcoin, gold, and the Nasdaq Index, data source: Coin Metrics and Google Finance

As the "anchor asset" of the entire cryptocurrency market, Bitcoin's pullback has spread to other assets. While privacy coins and other thematic sectors briefly outperformed, most coins remain highly correlated with Bitcoin.

Weakening Appeal of ETFs and DAT

Bitcoin's recent weakness partly stems from a decline in demand from core funding channels supporting its 2024-2025 trajectory. Since mid-October, ETFs have seen consecutive weeks of net outflows, totaling $4.9 billion, marking the largest redemption wave since Bitcoin dropped to $75,000 ahead of the April 2025 "Liberation Day" tariff announcement. Despite short-term outflows, on-chain holdings continue to trend upward, with BlackRock's IBIT ETF alone holding 780,000 Bitcoin, representing approximately 60% of the total spot Bitcoin ETF holdings.

If ETF inflows recover, it would signal stabilization in this channel. Historical data indicates that ETF demand has been a key force absorbing Bitcoin supply when risk appetite improves.

Weekly net inflows of Bitcoin ETFs, data source: Coin Metrics

Crypto Asset Treasuries (DATs) are also starting to face pressure. With the price correction, DAT firm stock values and crypto asset holdings have shrunk, putting pressure on the net asset value (NAV) premium that supports their growth engine. This has weakened the ability of DATs to acquire new capital through equity issuance or debt financing, thereby limiting the growth of their per-share crypto asset holdings. Smaller emerging DATs are especially sensitive to this, as changes in the market environment may make the cost basis and equity valuation no longer suitable for further accumulation.

The largest DAT by size currently—Strategy—holds 649,870 Bitcoin at an average cost of $74,333 (approximately 3.2% of Bitcoin's total current supply). As shown in the chart below, when Bitcoin's price rises and equity valuation is strong, Strategy's accumulation rate significantly accelerates, with a recent slowdown in accumulation pace. However, Strategy still holds unrealized gains, with its cost basis below the current market price.

If the price continues to drop or faces index exclusion risk, the Strategy may come under pressure; however, an improvement in the market environment is expected to enhance its balance sheet and valuation, creating a more favorable environment for DAT accumulation.

Strategy's Bitcoin purchase amount compared to the average cost basis, data source: Strategy and Bitbo Treasuries

This trend is in line with on-chain profit conditions. The short-term holders (holding period < 155 days) have seen their spent output profit ratio (SOPR) drop to around -23%, entering the loss zone, a level historically indicative of capitulation selling pressure from the most price-sensitive group. Long-term holders are still on average in a profitable state, but SOPR data shows a slight increase in profit-taking behavior. If the short-term SOPR rises above 1.0 while the long-term holders' selling pace slows down, it would signal a gradual market stabilization.

The Decentralization Process of Cryptocurrency: Perpetual Futures, DeFi Lending, and Liquidity

The "10.11" liquidation event initiated a multi-layered deleveraging cycle in futures, DeFi, and stablecoin collateralized leverage, the ongoing impact of which continues to unfold in the cryptocurrency market.

Deleveraging Purge in Perpetual Futures Markets

In a matter of hours, the perpetual futures market saw the largest forced liquidation event in history, with over a 30% reduction in the accumulated open interest (OI). Platforms that cater more to altcoins and retail traders (such as Hyperliquid, Binance, and Bybit) experienced the most significant drop in open interest, aligning with domains of leveraged concentration pre-deleveraging. As shown in the chart below, the current open interest level remains significantly below the pre-crash peak of over $90 billion and has seen a slight subsequent retracement, indicating that leverage within the system has been effectively cleared as the market stabilizes and readjusts.

Simultaneously, the funding rate has also weakened, reflecting a reset in bullish risk sentiment. Bitcoin's funding rate has recently hovered around neutral or slightly negative levels, in line with the market's ongoing lack of directional confidence.

Changes in perpetual contract open interest across exchanges, data source: Coin Metrics

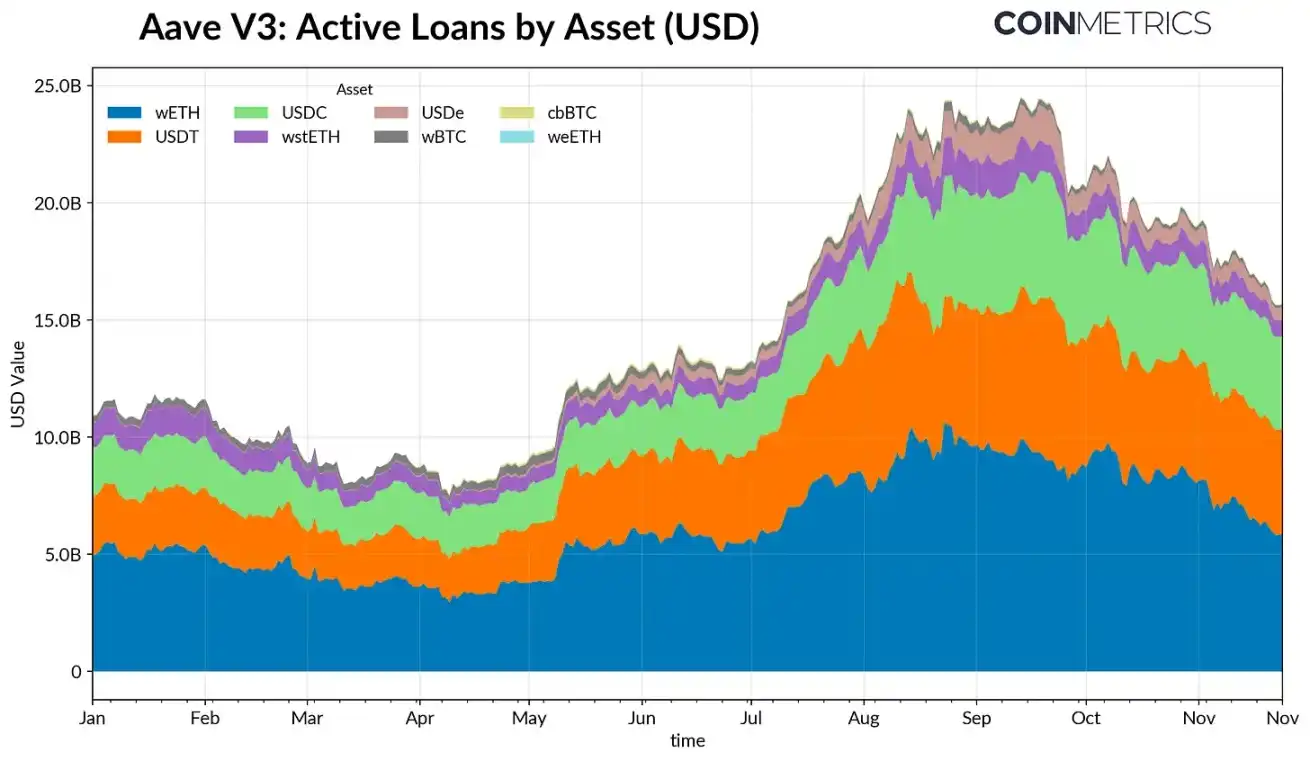

DeFi Deleveraging

The DeFi credit market has also undergone a gradual deleveraging process. Since reaching its peak at the end of September, the active loan size on Aave V3 has continued to decline. Against a backdrop of weak risk appetite and collateral repricing, borrowers have been reducing leverage and repaying debt. The most significant contraction in borrowing, denominated in stablecoins, was witnessed, with the USDe-related lending size plummeting by 65% due to the Ethena USDe de-pegging event, triggering a comprehensive liquidation of synthetic dollar leverage.

Ethereum-related borrowing has also contracted: the loan size for WETH and Liquidity Staking Tokens (LST) has decreased by around 35%-40%, reflecting a reduction in carry trade strategies and a shrinking of interest-bearing collateral strategies.

Aave V3 Active Loan Volume, Data Source: Coin Metrics

Lack of Spot Liquidity

Following the "10/11" liquidation event, spot market liquidity has remained tight. On major trading platforms, the trading depth of assets such as Bitcoin, Ethereum, Solana, etc., is still 30%-40% lower than early October levels within a ±2% range, indicating that liquidity has not yet recovered in line with prices. With a decrease in order book depth, the market remains fragile, and small trades can lead to disproportionate price fluctuations, exacerbating volatility and amplifying the impact of forced selling.

The liquidity situation for altcoins is even worse. Order book depth outside of mainstream assets has seen more severe and prolonged declines, reflecting continued risk aversion in the market and reduced market maker activity. A comprehensive improvement in spot liquidity will help reduce price shocks and stabilize the market, but to date, insufficient depth remains one of the most obvious signals that systemic pressures have not yet been fully relieved.

Exchange Order Book Depth Change, Data Source: Coin Metrics

Conclusion

The cryptocurrency market is undergoing a comprehensive adjustment, influenced by factors such as weak ETF and DAT demand, futures and DeFi market deleveraging, and a lack of spot liquidity. While these dynamics put pressure on prices, they also make the market system healthier, reduce leverage levels, make positions more neutral, and increasingly return to fundamentals.

At the same time, the macro environment remains a major obstacle. Softness in AI stocks, adjustments in interest rate expectations, and an overall risk-averse sentiment have dampened market demand. The market will remain in a tug-of-war between macro risk-off sentiment and the internal market structure of the cryptocurrency world until key funding channels (ETF inflows, DAT holdings, stablecoin supply growth) recover, and spot liquidity rebounds, laying the foundation for market stabilization and eventual reversal. Until then, the market will continue to navigate between macro risk-off sentiment and tensions in the cryptocurrency market structure.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Mars Morning News | Russia Plans to Ease Digital Asset Investment Thresholds, Expanding Legal Participation of Citizens in the Crypto Market

Russia plans to relax the investment threshold for digital assets, Texas allocates $5 million to Bitcoin ETF, an Ethereum whale sells 20,000 ETH, Arca's Chief Investment Officer says MSTR does not need to sell BTC, and the S&P 500 Index may rise by 12% next year. Summary generated by Mars AI. The accuracy and completeness of this summary produced by the Mars AI model are still being iteratively updated.

x402 The most crucial piece of the puzzle? Switchboard aims to rebuild the "oracle layer" from scratch

Switchboard is an oracle project within the Solana ecosystem and proposes to provide a data service layer for the x402 protocol. It adopts a TEE technology architecture, is compatible with x402 protocol standards, supports a pay-per-call billing model, and removes the API Key mechanism, aiming to build a trusted data service layer. Summary generated by Mars AI. The accuracy and completeness of this content, generated by the Mars AI model, is still in an iterative update phase.

Who would be the most crypto-friendly Federal Reserve Chair? Analysis of the candidate list and key timeline

Global markets are closely watching the change of Federal Reserve Chair: Hassett leading the race could trigger a crypto Christmas rally, while the appointment of hawkish Waller may become the biggest bearish factor.