Twilight of the Titans: How Has the Rise of Stablecoin Newcomers Eroded the Empires of Tether and Circle?

Solana provides Base with a $500 million annual "implicit subsidy," yet few people are aware of it.

Original Title: Apps and Chains, Not Issuers: The Next Wave of Stablecoin Economics Belongs to DeFi

Original Author: Simon, Delphi Digital

Original Translator: DingDang, Odaily Planet Daily

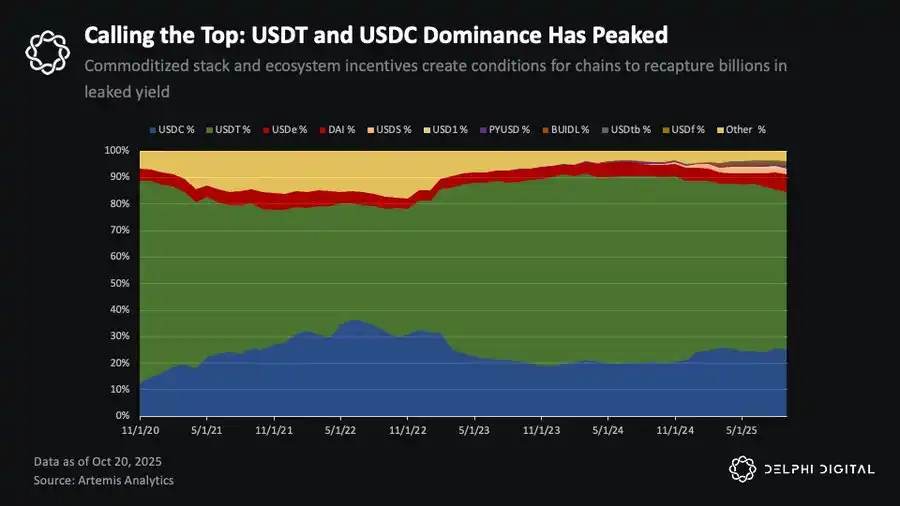

Tether and Circle's Moats Are Being Eroded: Distribution Channels Trump Network Effects. The stablecoin market share held by Tether and Circle may have peaked in relative terms, even as the overall stablecoin supply continues to grow. By 2027, the total market value of stablecoins is expected to surpass 1 trillion USD, but the gains from this expansion will not primarily flow to existing giants as they did in the last cycle. Instead, an increasing share will flow to "ecosystem-native stablecoins" and "white label issuance" strategies as blockchain and applications begin to internalize revenue and distribution channels.

Currently, Tether and Circle hold approximately 85% of the circulating stablecoin supply, totaling around 265 billion USD.

Background data is as follows: reportedly, Tether is being valued at 500 billion USD, raising 20 billion USD, with a circulation of around 185 billion USD, and Circle is valued at around 35 billion USD with a circulation of around 80 billion USD.

The network effects that supported their monopolistic positions are weakening. Three forces are driving this change:

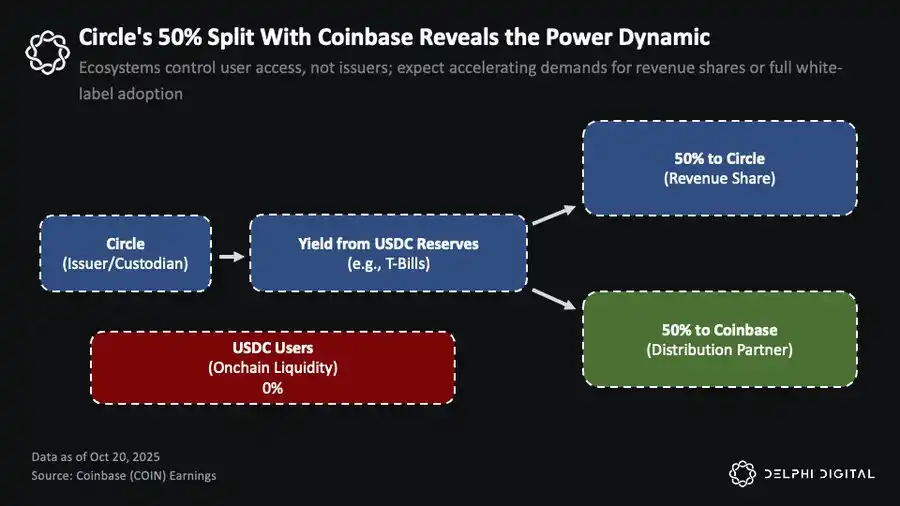

Firstly, the importance of distribution channels has surpassed the so-called network effects. The relationship between Circle and Coinbase illustrates this well. Coinbase obtains 50% of the residual yield from Circle's USDC reserves and monopolizes the revenue from all USDC on its platform. In 2024, Circle's reserve yield was around 1.7 billion USD, with approximately 908 million USD paid to Coinbase. This demonstrates that distribution partners of stablecoins can capture most of the economic benefits, explaining why players with strong distribution capabilities are now more inclined to issue their own stablecoins rather than continue to benefit the issuer.

Coinbase receives 50% of the interest from Circle's USDC reserve and exclusively captures the USDC interest held on the platform.

Secondly, cross-chain infrastructure makes stablecoins interchangeable. The official bridging upgrades of mainstream Layer 2, the general message passing protocol launched by LayerZero and Chainlink, and the maturity of smart routing aggregators have made stablecoin swaps between on-chain and cross-chain nearly costless and with a native user experience. Today, which stablecoin you use is no longer important as you can quickly switch based on liquidity demands. Not long ago, this was still a cumbersome process.

Thirdly, regulatory clarity is eliminating entry barriers. Legislation such as the GENIUS Act has established a unified framework for onshore stablecoins in the United States, reducing risks for infrastructure providers holding reserves. Meanwhile, an increasing number of white-label issuers are driving down the issuance fixed costs, and the treasury yields are providing a strong incentive for "float capital monetization." The result is that the stablecoin stack is being commoditized and is becoming increasingly homogeneous.

This commoditization has blurred the structural advantage of incumbents. Today, any platform with effective distribution capabilities can choose to "internalize" the stablecoin economy—instead of paying out interest to others. Early movers include fintech wallets, centralized exchanges, and an increasing number of DeFi protocols.

DeFi is where this trend is most evident and has the most profound impact.

From "Leakage" to "Yield": DeFi's New Stablecoin Playbook

This shift is already becoming apparent in the on-chain economy. Compared to Circle and Tether, many public chains and applications with stronger network effects (from product-market fit, user stickiness, distribution efficiency, among other metrics) are starting to adopt white-label stablecoin solutions to fully leverage their existing user base and capture the revenue that originally belonged to traditional issuers. For on-chain investors who have long overlooked stablecoins, this change is creating new opportunities.

Hyperliquid: The First "Defection" Within DeFi

This trend first emerged in Hyperliquid. At that time, approximately $5.5 billion in USDC was deposited on the platform—meaning that about $220 million in additional annual revenue flowed to Circle and Coinbase, rather than staying within Hyperliquid itself.

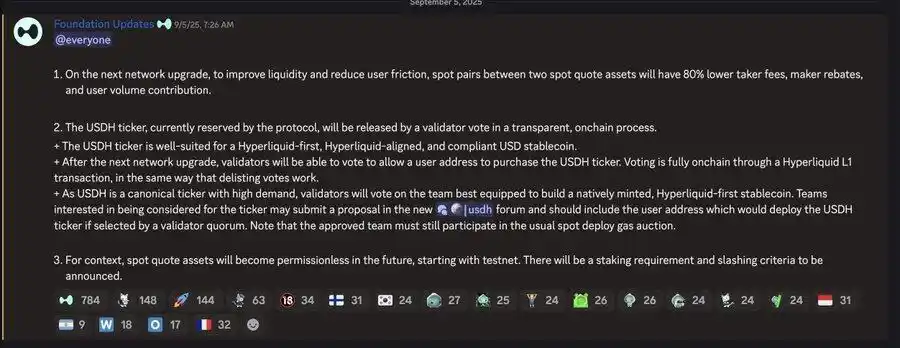

Prior to the validator vote determining USDH's code ownership, Hyperliquid announced the launch of a native, self-core issued asset.

For Circle, being the primary trading pair on various Hyperliquid core markets has brought significant revenue. They directly benefited from the exchange's explosive growth but hardly contributed value back to the ecosystem itself. For Hyperliquid, this meant a substantial loss of value to third parties with little to no contribution, severely contradicting its community-first, ecosystem-collaborative ethos.

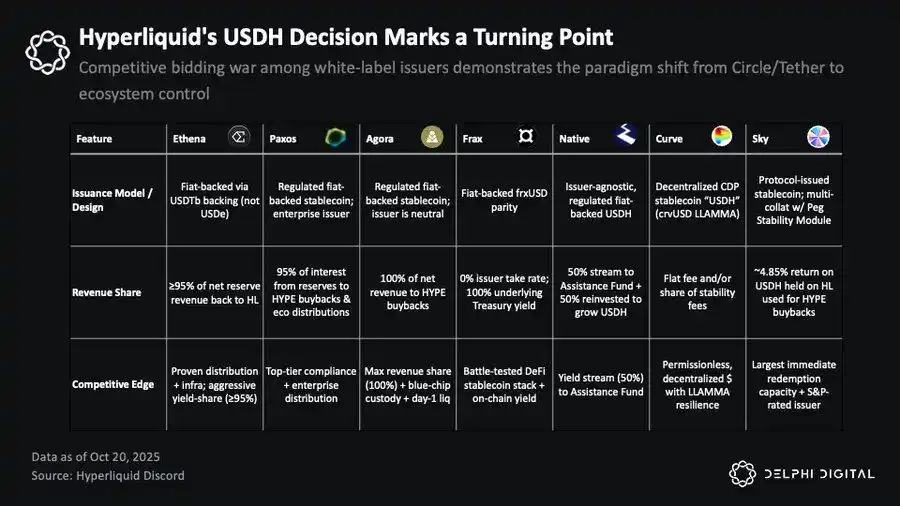

During the USDH bidding process, nearly all major white-label stablecoin issuers participated, including Native Markets, Paxos, Frax, Agora, MakerDAO (Sky), Curve Finance, and Ethena Labs. This marked the first large-scale competition at the application layer of the stablecoin economy, signaling a redefinition of the value of "distribution rights."

Ultimately, Native won the issuance rights for USDH—their proposal aligned more closely with the Hyperliquid ecosystem incentives. This model features issuer neutrality and compliance, with reserves managed offline by BlackRock and on-chain support provided by Superstate. Crucially, 50% of reserve earnings will be directly injected into Hyperliquid's relief fund, with the remaining 50% used to expand USDH liquidity.

While USDH will not replace USDC in the short term, this decision reflects a deeper power shift: in the DeFi space, moats and revenue are gradually moving towards applications and ecosystems with stable user bases and strong distribution capabilities, rather than traditional issuers like Circle and Tether.

White-Label Stablecoin Proliferation: Rise of the SaaS Model

Over the past few months, an increasing number of ecosystems have adopted the "white-label stablecoin" model. Ethena Labs' proposed "Stablecoin-as-a-Service" solution is at the forefront of this trend—on-chain projects like Sui, MegaETH, and Jupiter are either using or planning to issue proprietary stablecoins through Ethena's infrastructure.

The appeal of Ethena lies in its protocol that will directly reward holders. USDe's earnings come from basis trading. Although with a total supply exceeding $12.5 billion, the yield has compressed to about 5.5%, it is still higher than the U.S. Treasury bond yield (about 4%), and much better than the zero-yield status of USDT and USDC.

However, as other issuers start directly passing on Treasury bond yields to users, Ethena's relative advantage is decreasing—the Treasury-backed stablecoins are more attractive in terms of risk-reward ratio. If the rate-cut cycle continues, the basis trade spread will widen again, strengthening the appeal of such a "yield-driven model."

You might ask, does this violate the "GENIUS Act," which prohibits stablecoin issuers from directly paying yield to users? In fact, this restriction may not be as strict as imagined. The act does not explicitly prohibit third-party platforms or intermediaries from distributing rewards to stablecoin holders—as long as the source of the funds is provided by the issuer. This gray area has not been fully clarified, but many believe this "loophole" still exists.

Regardless of how regulation evolves, DeFi has always operated in a permissionless, edgy state and is likely to continue to do so in the future. What is more important than legal text is the economic reality behind it.

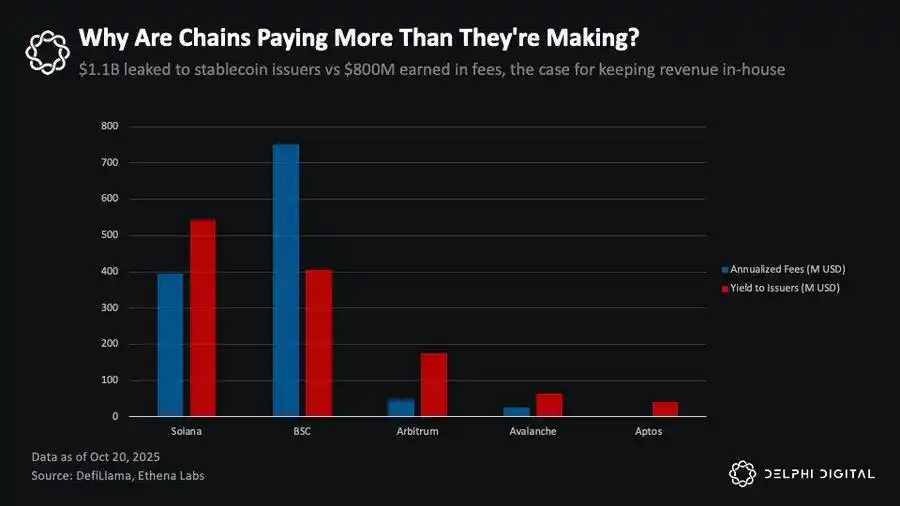

Stablecoin Tax: Earnings Drain on Mainstream Public Chains

Currently, about $30 billion of USDC and USDT is idle on Solana, BSC, Arbitrum, Avalanche, and Aptos. Based on a 4% reserve yield, this can generate approximately $1.1 billion in interest income for Circle and Tether annually. This number is about 40% higher than the total transaction fee income of these public chains. This also highlights a reality: Stablecoins are becoming the largest but not yet fully monetized value layer in L1, L2, and various applications.

Taking Solana, BSC, Arbitrum, Avalanche, and Aptos as examples, Circle and Tether earn about $1.1 billion in annual revenue, while these ecosystems only earn $800 million in transaction fees.

In simple terms, these ecosystems are losing hundreds of millions of dollars in stablecoin revenue every year. Even if only a small part of it is left on-chain to capture on its own, it is enough to reshape its economic structure—providing a public chain with a more robust, countercyclical income base than transaction fees.

What is preventing them from reclaiming these revenues? The answer is: nothing. In fact, there are many paths to take. They can negotiate revenue sharing with Circle, Tether (as Coinbase did); they can initiate a competitive bidding process with white-label issuers like Hyperliquid; or they can launch a native stablecoin through "Stablecoin-as-a-Service" platforms like Ethena.

Of course, each path has its trade-offs: partnering with a traditional issuer can maintain the familiarity, liquidity, and stability of USDC or USDT, assets that have withstood multiple market cycles and maintained trust in extreme stress tests; issuing a native stablecoin increases control and potential revenue but faces a cold start problem. Both approaches have their corresponding infrastructure, and each chain can choose a path based on its priorities.

Redefining Public Blockchain Economics: Stablecoins as a New Revenue Engine

Stablecoins have the potential to become the primary source of revenue for certain public blockchains and applications. Today, when the blockchain economy relies solely on transaction fees, growth faces a structural limit—network revenue can only increase when users "pay more fees," which conflicts with the goal of "lowering barriers to use."

The USDm project of MegaETH is a response to this. By partnering with Ethena to issue a white-label stablecoin USDm, with BlackRock's on-chain treasury bond product BUIDL as the reserve asset, MegaETH can operate a sequencer at cost and reinvest the revenue into community initiatives by internalizing USDm revenue. This model gives the ecosystem a sustainable, low-cost, and innovation-friendly economic structure.

The top DEX aggregator on Solana, Jupiter, is pursuing a similar strategy through JupUSD. It plans to deeply integrate JupUSD into its product suite—from the collateral assets of Jupiter Perpetual Contracts (Jupiter Perps) (where the approximately $750 million stablecoin reserve will gradually be replaced) to the liquidity pools of Jupiter Lend. Through this strategy, Jupiter aims to have the stablecoin revenue flow back into its ecosystem, whether it is used to reward users, buy back tokens, or fund incentive programs. The value accumulation brought by these revenue streams far outweighs handing over all revenue to external stablecoin issuers.

This is the core shift happening right now: Those who used to passively contribute to the old issuer's revenue are now applying it to actively recapture value on the public chain.

Mismatched Valuations Between Applications and Public Chains

As all of this unfolds, I believe that both public chains and applications are embarking on a path toward generating more sustainable income, which will gradually move away from the "Internet capital market" and on-chain speculative activities' cyclical fluctuations. If so, they may finally find rationality for the often-questioned "out-of-touch with reality" high valuations.

The valuation frameworks most people still use mainly view these two levels from the perspective of "the total economic activity happening on top of them." In this model, on-chain fees represent the total cost borne by users, and the chain's revenue is the portion of these fees flowing to the protocol itself or token holders (e.g., through mechanisms like burning, treasury inflows, etc.). However, this model has had issues from the start—it assumes that as long as there is activity, the public chain will inevitably capture value, even if the actual economic benefits have already flown elsewhere.

Today, this model is starting to shift, led by the application layer. The most straightforward example is the two star projects of this cycle: Pump.fun and Hyperliquid. Both of these applications allocate almost 100% of their revenue (note, not fees) towards buying back their own tokens, while their valuation multiples are significantly lower than the primary infrastructure layer. In other words, these applications are generating real and transparent cash flow, not imaginary implicit returns.

In contrast, the market-to-sales ratios of most mainstream public chains still reach hundreds or even thousands, while leading applications achieve higher returns at lower valuations.

Take Solana, for example. In the past year, the chain's total fees were around $632 million, revenue around $1.3 billion, market cap around $105 billion, and fully diluted valuation (FDV) around $118.5 billion. This means Solana's market cap to fee ratio is around 166x, market cap to revenue ratio around 80x—this is already a relatively conservative valuation for a large L1. Many other public chains have FDV valuation multiples reaching even thousands.

In comparison, Hyperliquid created $667 million in revenue, FDV of $38 billion, corresponding multiples of 57x based on FDV and only 19x based on circulating market cap. Pump.fun's revenue is $724 million, FDV multiples are only 5.6x, and market cap multiples are just 2x. Both of these demonstrate: Applications highly aligned with the product and strong distribution capabilities are creating significant income at multiples much lower than the base layer.

This is an ongoing power shift. The valuation of applications is increasingly dependent on the real revenue they generate and return to the ecosystem, while the base layer is still struggling to find the rationale behind its valuation. The continuously diminishing L1 premium is the clearest signal.

Unless the base layer can find a way to "internalize" more value from within the ecosystem, these inflated valuations will continue to be compressed. "White-label stablecoins" may be the first step public chains take to reclaim some of that value—turning what was once a passive "monetary channel" into an active revenue layer.

Coordination Problem: Why Some Public Chains Move Faster

The shift towards a "stablecoin aligned with the ecosystem's interests" is already underway; the significant differences in advancement speed between various public chains stem from their coordination capabilities and execution urgency.

For example, Sui—although its ecosystem is far less mature than Solana's—is moving at a rapid pace. Sui is collaborating with Ethena to introduce both sUSDe and USDi stablecoins simultaneously (the latter similar to the BUIDL-supporting stablecoin mechanism being explored by Jupiter and MegaETH). This is not a spontaneous action at the application layer but a strategic decision at the base layer: to internalize the stablecoin economy early, before path dependence sets in. Although these products are expected to launch officially in Q4, Sui is the first mainstream public chain to actively pursue this strategy.

In contrast, Solana faces a more complex and painful situation. Currently, there are around $15 billion in stablecoin assets on the Solana blockchain, with over $10 billion being USDC. These funds generate approximately $500 million in interest income for Circle annually, with a significant portion flowing back to Coinbase through profit-sharing agreements.

And where does Coinbase use these profits?—To subsidize Base, one of Solana's direct competitors. Part of Base's liquidity incentives, developer grants, ecosystem investments, and other funds come from the $10 billion in USDC on Solana. In other words, Solana is not only losing income but is also providing blood transfusions to its competitors.

This issue has long been a topic of strong interest within the Solana community. For example, Helius founder @0xMert_ called for Solana to launch a stablecoin tied to the ecosystem's interests and suggested using 50% of the revenue for SOL buybacks and burns. Senior members of some stablecoin issuers (such as Agora) have also proposed similar solutions, but compared to Sui's proactive approach, the Solana official response has been relatively lukewarm.

The reason is actually not very complicated: as regulatory frameworks such as the GENIUS Act have gradually become clearer, stablecoins have become more and more "commoditized." Users don't care whether they hold USDC, JupUSD, or any other compliant stablecoin—just as long as the price is pegged stable and there is sufficient liquidity. So, why default to using a stablecoin that is funneling profits to a competitor?

One reason Solana seems hesitant on this issue is that it wants to maintain "trusted neutrality." This is particularly important as the foundation strives for institutional legitimacy—after all, the only ones currently truly recognized in this regard are Bitcoin and Ethereum. To attract heavyweight issuers like BlackRock, this "institutional endorsement" not only brings in real capital but also grants asset "commoditization" status in the eyes of traditional finance—Solana must keep a certain distance from ecosystem politics. If it publicly supports a specific stablecoin, even if it's "eco-friendly," Solana may run into trouble in its journey to this level, or even be seen as favoring certain ecosystem participants.

Additionally, the scale and diversity of the Solana ecosystem make the situation even more complex. Hundreds of protocols, thousands of developers, tens of billions in TVL. At this scale, coordinating the entire ecosystem to "abandon USDC" becomes exponentially more challenging. Yet, this complexity ultimately becomes a feature, reflecting the maturity of the network and the depth of its ecosystem. The real issue is: inaction also comes at a cost, and that cost will continue to grow.

Path dependence accumulates daily. Every new user defaulting to USDC is increasing the future switching costs. Every protocol optimizing liquidity around USDC makes it harder for alternative solutions to launch. From a technical perspective, migrating existing infrastructure can be done almost overnight—the real challenge lies in coordination.

Currently within Solana, Jupiter is taking the lead by introducing JupUSD, committing to channel profits back into the Solana ecosystem, deeply integrating it into its product suite. The question now is: will other leading applications follow suit? Will platforms like Pump.fun also adopt a similar strategy, internalizing stablecoin earnings? At what point will Solana have no choice but to intervene from the top down, or will it simply let the applications built on top of it collect these profits themselves? From a public chain perspective, if apps can retain stablecoin economic benefits, although not the most ideal outcome, it's still better than having those benefits flow off-chain or even to enemy camps.

Ultimately, from the perspective of a public blockchain or a wider ecosystem, this game requires collective action: protocols need to tilt their liquidity towards a common stablecoin, treasuries need to make thoughtful allocation decisions, developers should change the default user experience, and users must use their own funds to "vote." The $500 million annual subsidy that Solana provides to Base will not disappear due to a foundation's mere statement; it will only truly disappear at the moment when ecosystem participants "refuse to continue funding competitors."

Conclusion: Power Shift from Issuer to Ecosystem

The next phase of stablecoin economics will no longer depend on who issues the token, but on who controls the distribution channels, and who can coordinate resources and capture market share at a faster pace.

Circle and Tether were able to build massive business empires relying on "first-mover advantage" and "liquidity bootstrapping." However, as the stablecoin stack gradually commodifies, their moats are being eroded. Cross-chain infrastructure allows for almost seamless interchangeability between different stablecoins; regulatory clarity reduces entry barriers; white-label issuers drive down issuance costs. Most importantly, platforms with the strongest distribution capabilities, high user stickiness, and mature monetization models have begun internalizing revenue—no longer paying interest and profits to third parties.

This change is already underway. Hyperliquid, by pivoting to USDH, is reclaiming the $220 million annual revenue stream that used to flow to Circle and Coinbase; Jupiter is deeply integrating JupUSD liquidity into its entire product suite; MegaETH is operating its sequencer at near cost using stablecoin revenue; Sui, before path dependence sets in, collaborated with Ethena to launch an ecosystem-aligned stablecoin. These are just the trailblazers. Today, every public chain bleeding hundreds of millions of dollars annually to Circle and Tether has a replicable template to follow.

For investors, this trend provides a new perspective for ecosystem evaluation. The key question is no longer: "How much activity is happening on this chain?" but rather: "Can it overcome coordination challenges, achieve liquidity pool monetization, and capture stablecoin yields at scale?" As public chains and applications begin to "capture" hundreds of millions of dollars in annualized revenue into their systems, used for token buybacks, ecosystem incentives, or protocol fees, market participants can directly "leverage" these cash flows through these platforms' native tokens. Protocols and applications capable of internalizing this portion of revenue will have more robust economic models, lower user costs, and a more aligned interest with the community; while projects that fail to do so will continue to pay the "stablecoin tax," watching their valuations being compressed.

The most interesting opportunity in the future lies not in holding equity in Circle, nor in betting on those high Market Cap Issuer Tokens. The real value is in: identifying which chains and applications can accomplish this transition, turning the "passive financial pipeline" into an "active revenue engine". Distribution is the new moat. Those who control the "flow of funds", rather than just laying down the "funds channel", will define the landscape of the next phase of the stablecoin economy.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gain Insight into Cryptocurrency’s Promising Future for 2026

In Brief The next major crypto bull cycle will start in early 2026. Institutional investors and regulation drive long-term market confidence. Short-term shifts show investors favoring stablecoins amid volatility.

Stunning $204 Million USDT Transfer Ignites Market Speculation