Market share plummets by 60%, can Hyperliquid return to the top with HIP-3 and Builder Codes?

What has Hyperliquid experienced recently?

Original Title: Hyperliquid Growth Situation

Original Author: @esprisi0

Translation: Peggy, BlockBeats

Editor's Note: Hyperliquid once dominated the decentralized derivatives sector, but its market share plummeted sharply in the second half of 2025, drawing industry attention: has it peaked, or is it laying out the next stage? This article reviews Hyperliquid’s three phases: from extreme dominance with a market share as high as 80%, to a loss of momentum dropping to 20% due to strategic transformation and intensified competition, and finally to a resurgence centered on HIP-3 and Builder Codes.

The following is the original text:

In recent weeks, concerns about Hyperliquid’s future have been mounting. The loss of market share, rapidly rising competitors, and an increasingly crowded derivatives sector have raised a key question: what is really happening beneath the surface? Has Hyperliquid already peaked, or is the current narrative overlooking deeper structural signals?

This article will break it down step by step.

Phase One: Extreme Dominance

From early 2023 to mid-2025, Hyperliquid continuously set new historical highs on key metrics and steadily increased its market share, thanks to several structural advantages:

An incentive mechanism based on points attracted massive liquidity; a first-mover advantage in launching new perpetual contracts (such as $TRUMP, $BERA) made Hyperliquid the most liquid venue for new trading pairs and the preferred platform for pre-listing trading (such as $PUMP, $WLFI, XPL). To avoid missing emerging trends, traders were compelled to flock to Hyperliquid, pushing its competitive edge to the peak; among all perpetual DEXs, it offered the best UI/UX experience; fees were lower than centralized exchanges (CEX); spot trading was launched, unlocking new use cases; Builder Codes, HIP-2, and HyperEVM integration; and even during major market crashes, it achieved zero downtime.

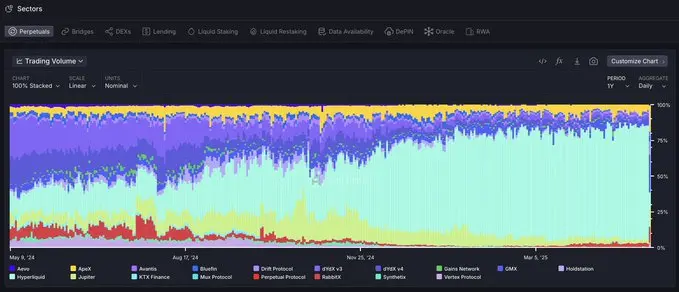

As a result, Hyperliquid’s market share grew continuously for over a year, reaching a peak of 80% in May 2025.

According to perpetual contract trading volume market share data provided by @artemis

At that stage, the Hyperliquid team was clearly ahead of the entire market in terms of innovation and execution speed, with no truly comparable products in the entire ecosystem.

Phase Two: The Rise of the "AWS of Liquidity" and Accelerated Competition

Since May 2025, Hyperliquid’s market share has plummeted, dropping from about 80% to nearly 20% of trading volume by early December.

@HyperliquidX market share (data source: @artemis)

This relative loss of momentum compared to competitors can be attributed to several factors:

Strategic Shift from B2C to B2B

Hyperliquid did not double down on the pure B2C model, such as launching its own mobile app or continuously rolling out new perpetual contract products, but instead chose to shift to a B2B strategy, positioning itself as the "AWS of liquidity".

This strategy focused on building core infrastructure for external developers to use, such as Builder Codes for the frontend and HIP-3 for launching new perpetual markets. However, this transformation essentially handed over the initiative for product deployment to third parties.

In the short term, this strategy was not ideal for attracting and retaining liquidity. The infrastructure is still in its early stages, adoption takes time, and external developers do not yet have the distribution capabilities and trust that the Hyperliquid core team has built up over the long term.

Competitors Seize the Opportunity During Hyperliquid’s Transition

Unlike Hyperliquid’s new B2B model, competitors have maintained full vertical integration, allowing them to significantly accelerate the launch of new products.

Since they do not need to delegate execution, these platforms retain full control over product releases and can quickly expand by leveraging their established user trust. As a result, they are more competitive than they were in the first phase.

This directly translates into market share growth. Competitors now not only offer all the products available on Hyperliquid, but also launch features that HL has not yet rolled out (for example, Lighter has launched spot markets, perpetual stocks, and forex).

Incentives and "Mercenary Liquidity"

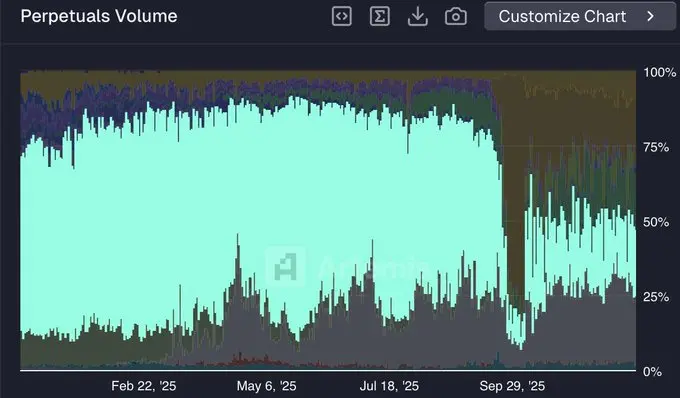

Hyperliquid has not run any official incentive programs for over a year, while its main competitors remain active. Lighter, which currently leads in trading volume market share (about 25%), is still in its pre-TGE points season.

@Lighter_xyz market share (data source: @artemis)

In DeFi, liquidity is more "mercenary" than anywhere else. A significant portion of the trading volume flowing from Hyperliquid to Lighter (and other platforms) is likely driven by incentives and related to airdrop farming. As with most perpetual DEXs running points seasons, Lighter’s market share is expected to decline after TGE.

Phase Three: The Rise of HIP-3 and Builder Codes

As mentioned earlier, building the "AWS of liquidity" is not the optimal short-term strategy. However, in the long run, this model precisely positions Hyperliquid to become the core hub of global finance.

Although competitors have already copied most of Hyperliquid’s current features, true innovation still originates from Hyperliquid. Developers building on Hyperliquid benefit from domain specialization and can formulate more targeted product development strategies on top of the ever-evolving infrastructure. In contrast, protocols like Lighter, which remain fully vertically integrated, will face limitations when optimizing multiple product lines simultaneously.

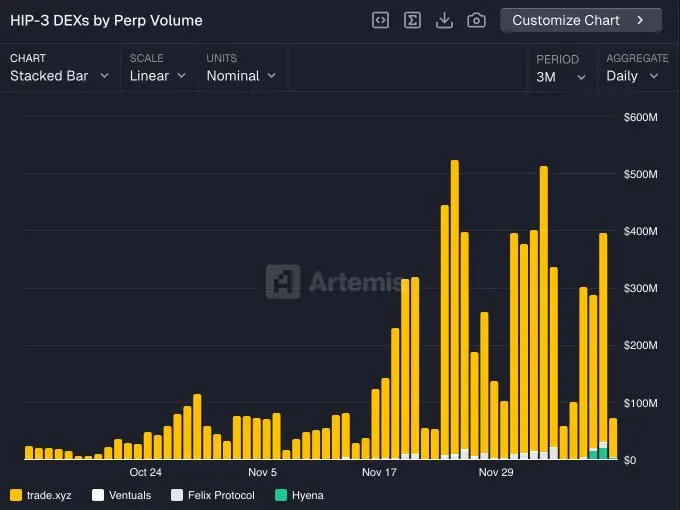

HIP-3 is still in its early stages, but its long-term impact has already begun to show. The main participants include:

@tradexyz has launched perpetual stocks

@hyenatrade recently deployed a trading terminal for USDe

More experimental markets are emerging, such as @ventuals offering pre-IPO exposure, and @trovemarkets targeting niche speculative markets like Pokémon or CS:GO assets

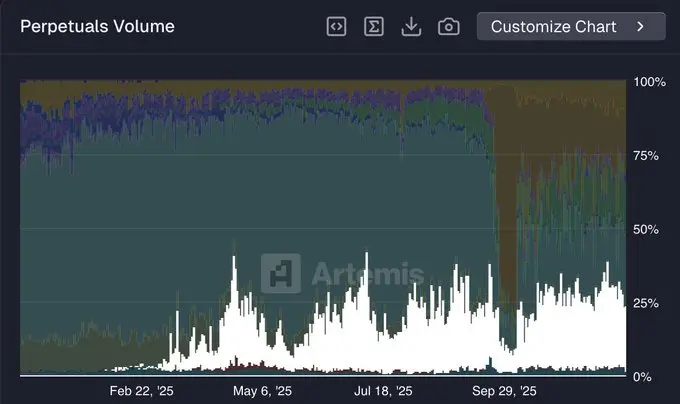

It is expected that by 2026, HIP-3 markets will account for a significant share of Hyperliquid’s total trading volume.

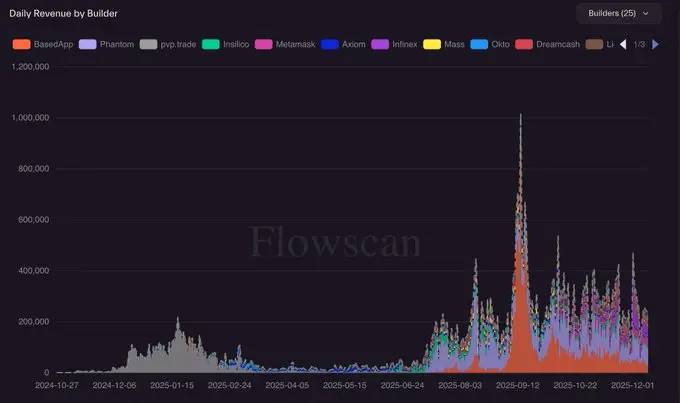

HIP-3 trading volume (by Builder)

The key driver that will ultimately restore Hyperliquid’s dominance is the synergy between HIP-3 and Builder Codes. Any frontend integrated with Hyperliquid can instantly access the full HIP-3 market, thus offering users unique products.

Therefore, developers are strongly motivated to launch markets via HIP-3, as these markets can be distributed on any compatible frontend (such as Phantom, MetaMask, etc.) and tap into entirely new sources of liquidity. This is a perfect virtuous cycle.

The continued development of Builder Codes makes me more optimistic about the future, both in terms of revenue growth and active user growth.

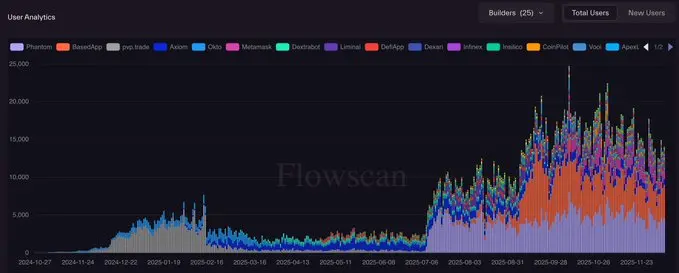

Builder Codes revenue (data source: @hydromancerxyz)

Builder Codes daily active users (data source: @hydromancerxyz)

Currently, Builder Codes are mainly used by crypto-native applications (such as Phantom, MetaMask, BasedApp, etc.). However, I expect that in the future, a new class of super apps built on Hyperliquid will emerge, aiming to attract a completely non-crypto-native user base.

This is likely to become the key path for Hyperliquid to scale up to the next stage, and will also be the focus of my next article.

[ Original Link ]

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The $150,000 Collective Illusion: Why Did All Mainstream Institutions Misjudge Bitcoin in 2025?

There is a significant discrepancy between the expected and actual performance of the bitcoin market in 2025. Institutional forecasts have collectively missed the mark, mainly due to incorrect assessments of ETF inflows, the halving cycle effect, and the impact of Federal Reserve policies. Summary generated by Mars AI. The accuracy and completeness of this summary are still being iteratively improved by the Mars AI model.

JPMorgan Chase: Oracle's aggressive AI investment sparks concerns in the bond market.

Aster launches Shield Mode: a high-performance trading protection mode designed for on-chain traders

This trading feature, as an innovative protection mode, is dedicated to integrating the full 1001x leveraged trading experience into a faster, safer, and more flexible on-chain trading environment.

Crypto industry leaders gather in Abu Dhabi, calling the UAE the "new Wall Street of crypto"

Banding together during the bear market to embrace major investors!