On the eve of the interest rate decision, hawkish rate cuts loom, putting the liquidity gate and the crypto market to the year-end test

A divided Federal Reserve and a possible "hawkish" rate cut.

A Divided Federal Reserve and a Possible "Hawkish" Rate Cut

Written by: ChandlerZ, Foresight News

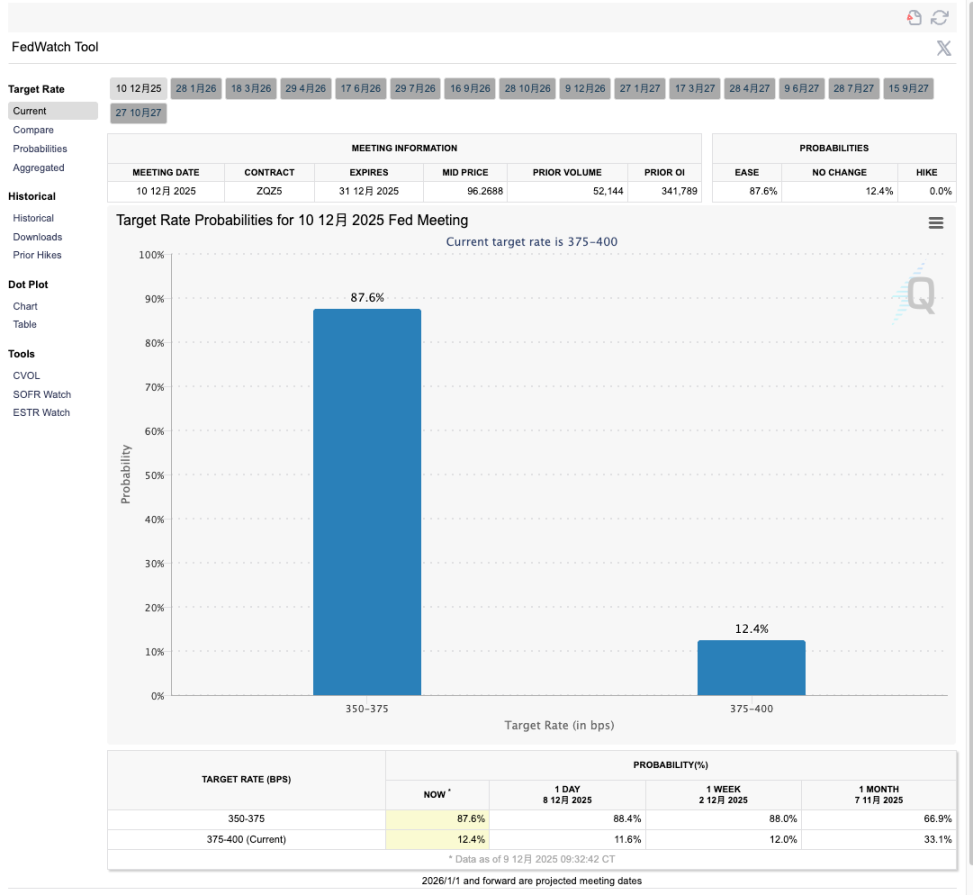

In the early morning of December 11, East 8th District time, the Federal Reserve will announce its final interest rate decision of the year. The market has almost reached a consensus that the federal funds target range is highly likely to be lowered by another 25 basis points, from 3.75%–4.00% to 3.50%–3.75%, marking the third rate cut since September.

But rather than waiting to see if there will be a rate cut, the market seems more concerned about whether this will be a standard "hawkish" rate cut.

Behind this subtle sentiment is a highly divided Federal Open Market Committee. Some members worry that the labor market is already showing signs of weakness amid government shutdowns and proactive corporate downsizing, and keeping rates high will only amplify recession risks; other members are focused on core inflation, which remains above the 2% target, believing that current rates are already sufficiently restrictive and that turning to easing too early will sow greater inflation risks for the future.

What makes things trickier is that this debate is happening during a data vacuum. The U.S. government shutdown has delayed the release of some key macroeconomic data, forcing the FOMC to make decisions with incomplete information, which also makes policy communication at this meeting significantly more challenging than usual.

A Divided FOMC and a Reprise of the Hawkish Rate Cut

If this rate-setting meeting is seen as a major drama, then the hawkish rate cut in October serves as the prologue. At that time, the Federal Reserve lowered the federal funds rate target range by 25 basis points and simultaneously announced the official end of the three-year quantitative tightening process from December 1, halting further balance sheet reduction. Operationally, this was a clearly dovish combination—rate cuts plus stopping balance sheet reduction—which should, in theory, provide sustained support for risk assets.

However, at the time, Powell repeatedly poured cold water during the press conference. He emphasized that another rate cut in December was by no means a foregone conclusion and, unusually, publicly mentioned strong internal disagreements within the committee. As a result, while rates did fall and the Fed signaled marginal monetary easing, both the dollar and U.S. Treasury yields climbed, and stocks and crypto assets quickly gave back their gains after a brief spike.

New York Fed President Williams stated clearly at the end of November that there was still room for further adjustments to the federal funds rate target range in the short term, which was seen as a public endorsement of this rate cut; in contrast, several officials, including those from the Boston Fed and Kansas City Fed, repeatedly reminded that current inflation remains above the 2% target and that service prices are particularly sticky, so there is no strong need to continue easing in this environment. In their view, even if there is another rate cut this time, it is more like a minor policy adjustment rather than the start of a new easing cycle.

External institutions' forecasts also reflect this ambivalence. Investment banks such as Goldman Sachs generally expect the dot plot to slightly raise the path of rate cuts after 2026, meaning that while acknowledging current economic growth and employment pressures, the Fed will still deliberately signal to the market not to interpret this rate cut as a return to a continuous easing mode.

Three Scenarios: How Bitcoin Is Priced in the Macro Gap

On the eve of the rate decision, bitcoin finds itself in a rather delicate position. After surging in October, its price underwent a roughly 30% pullback and is now consolidating above $90,000; meanwhile, ETF net inflows have slowed significantly compared to the early-year peak, some institutions have begun to lower their medium- and long-term target prices, and concerns about persistently high risk-free rates are slowly seeping into pricing models. The signals from this rate meeting could very well push the market onto three completely different trajectories.

The first, and most likely, is the baseline scenario: rates are cut by another 25 basis points as expected, but the dot plot is conservative about the number of rate cuts in 2026 and beyond, and Powell continues to stress at the press conference that there is no preset path for continuous rate cuts and everything depends on the data. In this scenario, the market still has reason to buy the rate cut itself in the short term, and bitcoin may attempt to break through resistance near previous highs that night. However, as long-term U.S. Treasury yields stabilize or even rise slightly, real rates will increase, and the sustainability of the sentiment recovery will be tested. Prices are more likely to see repeated tug-of-war at high levels rather than a one-way trend surge.

The second, a relatively dovish but less likely surprise scenario: in addition to the rate cut, the dot plot significantly lowers the medium-term rate center, suggesting there is room for more than two rate cuts in 2026, and the post-meeting statement positions the end of balance sheet reduction more as a reserve management-type bond purchase, with a clearer commitment to maintaining ample reserves. Essentially, this scenario is another rate cut plus a reversal in liquidity expectations, which would be a substantial positive for all long-duration assets.

For the crypto market, as long as bitcoin can hold its ground near $90,000, it has a chance to challenge the psychological $100,000 mark again, while on-chain assets represented by ETH and mainstream DeFi and L2 protocols could see significant excess returns driven by a return of on-chain liquidity.

The third is an unexpected scenario that would significantly suppress market risk appetite: the Fed chooses to hold steady, or, although it cuts rates, the dot plot sharply raises long-term rates and significantly reduces the number of future rate cuts, sending a signal that October and December were just insurance adjustments and that high rates will remain the main theme for longer. In this scenario, the dollar and U.S. Treasury yields are likely to strengthen, and all non-cash-flow assets that rely on valuation support will come under pressure.

Given that bitcoin has already experienced a significant pullback, ETF inflows are slowing, and some institutions are adjusting their expectations, the addition of a negative macro narrative could technically lead to a search for new support levels. High-leverage and purely narrative-driven altcoin sectors are even more likely to become the first targets for liquidation in this environment.

For crypto market participants, this rate decision night is more like a macro-level options expiry date.

Whether in U.S. stocks or bitcoin history, most FOMC rate decision nights follow a similar rhythm. The hour after the decision is announced is the battlefield for emotions, algorithms, and liquidity, with wild swings in candlesticks but no stable directional signal; the real trend usually only emerges after the press conference ends and investors have digested the dot plot and economic forecasts, gradually becoming apparent over the next 12–24 hours.

The rate decision determines the current tempo, while the direction of liquidity is likely to decide the second half of this cycle.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The largest IPO in history! SpaceX reportedly seeks to go public next year, aiming to raise over 30 billion and targeting a valuation of 1.5 trillion.

SpaceX is advancing its IPO plan, aiming to raise significantly more than $30 billion, which could make it the largest public offering in history.

DiDi has become a digital banking giant in Latin America

Attempting to directly replicate the "perfect model" used domestically will not work; we can only earn respect by demonstrating our ability to solve real problems.

Macroeconomic structural contradictions are deepening, but is it still a good time for risk assets?

In the short term, risk assets are viewed bullishly due to AI capital expenditures and affluent consumer spending supporting earnings. However, in the long term, caution is advised regarding structural risks brought by sovereign debt, demographic crises, and geopolitical restructuring.

a16z predicts four major trends will be announced first in 2026

AI is driving a new round of structural upgrades in infrastructure, enterprise software, health ecosystems, and virtual worlds.