Investing in top VCs for four years, but the principal is halved: Has the myth of crypto funds collapsed?

Author: PANews, Zen

Original Title: Principal Halved After Four Years Investing in Top VC, What’s Wrong with Crypto Funds?

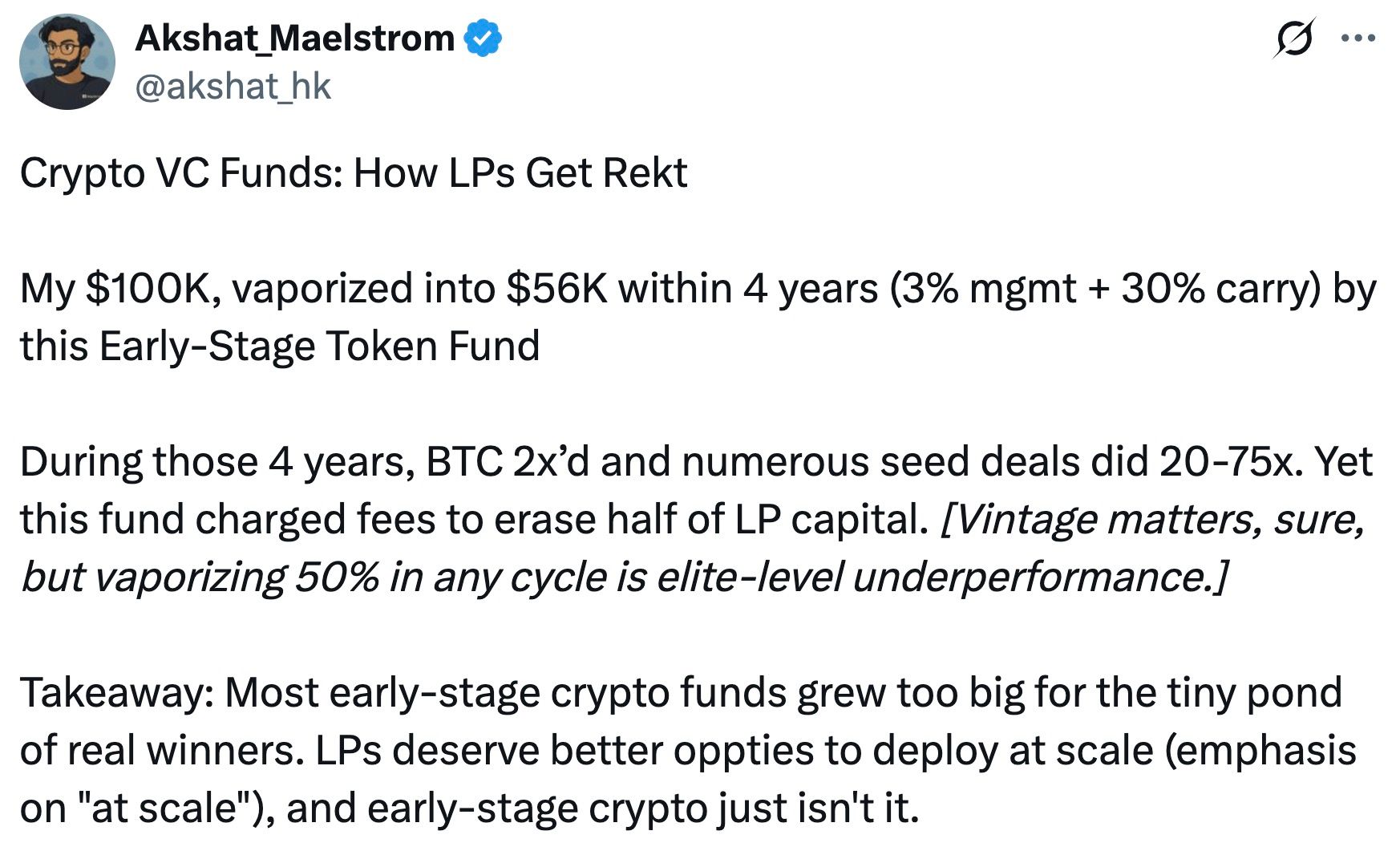

Recently, Akshat Vaidya, co-founder and Chief Investment Officer of Arthur Hayes’ family office Maelstrom, publicly disclosed a dismal investment performance on X, sparking widespread discussion within the crypto community.

Vaidya stated that four years ago, he invested $100,000 in Pantera Capital’s early-stage token fund (Pantera Early-Stage Token Fund LP), which is now worth only $56,000, nearly half of his principal lost.

By comparison, Vaidya pointed out that during the same period, the price of bitcoin roughly doubled, and the investment returns of many seed-round crypto projects even soared by 20–75 times. Vaidya lamented: “Although the specific year you enter the market matters, losing 50% in any cycle is the worst performance.” This sharp comment directly questioned the fund’s performance and triggered heated debate in the industry about the performance and fee models of large crypto funds.

The “3/30” Era of Market Frenzy

Vaidya specifically mentioned and criticized the “3/30” fee structure, which refers to an annual 3% management fee and a 30% performance fee on investment returns. This is significantly higher than the traditional “2/20” model commonly seen in hedge funds and venture capital funds, i.e., a 2% management fee and 20% performance fee.

At the peak of the crypto market frenzy, some well-known institutional funds, leveraging their extensive project pipelines and track records, charged investors fees above traditional standards, such as a 2.5% or 3% management fee and a 25% or even 30% performance fee. Pantera, which Vaidya criticized, is a typical example of high fees.

As the market has evolved, crypto fund fee rates have also gradually changed in recent years. After enduring bull and bear cycles, and under pressure from LPs and fundraising challenges, crypto funds are generally moving toward lower fee structures. Newly raised crypto funds in recent years have started to make concessions on fees, such as lowering management fees to 1–1.5% or only charging higher performance fees on excess returns, in an attempt to better align with investors’ interests.

Currently, crypto hedge funds typically use the classic “2% management fee and 20% performance fee” structure, but capital allocation pressures have led to a decrease in average fees. According to data released by Crypto Insights Group, current management fees are close to 1.5%, while performance fees, depending on strategy and liquidity, tend to range from 15% to 17.5%.

Crypto Funds Struggle to Scale

Vaidya’s post also sparked discussion about the scale of crypto funds. Vaidya bluntly stated that, with few exceptions, large crypto venture funds generally deliver poor returns and are detrimental to limited partners. He said the purpose of his post was to use data to remind/educate everyone that crypto venture capital cannot be scaled, even for well-known brands with top investors.

Some support his view, believing that early crypto funds raising too much capital has actually become a drag on performance. Top institutions like Pantera, a16z Crypto, and Paradigm have raised multi-billion dollar crypto funds in recent years, but deploying such massive capital efficiently in a relatively early-stage crypto market is extremely difficult.

With a limited pool of projects, large funds are forced to “cast a wide net” by investing in numerous startups, resulting in low allocation per project and mixed quality, with excessive diversification making it hard to achieve outsized returns.

In contrast, smaller funds or family offices, due to their moderate capital size, can more strictly screen projects and focus on high-quality investments. Supporters believe that this “small and refined” strategy is more likely to outperform the market. Vaidya himself also commented that he agrees more with the view that “the problem is not early-stage tokens, but fund size,” and that “the ideal early-stage crypto fund must be small and flexible.”

However, there are dissenting voices questioning this radical view. They argue that while large funds may face diminishing marginal returns when chasing early-stage projects, their value to the industry should not be completely negated by a single poor investment. Large crypto funds often have abundant resources, professional teams, and extensive industry networks, allowing them to provide value-added services to projects post-investment and promote the development of the entire ecosystem—something individual investors or small funds can hardly match.

In addition, large funds can usually participate in larger financing rounds or infrastructure projects, bringing the deep capital support needed by the industry. For example, some public chains, trading platforms, and other projects requiring hundreds of millions of dollars in financing cannot do without the participation of large crypto funds. Therefore, large funds have their rationality, but should control fund size to match market opportunities and avoid overexpansion.

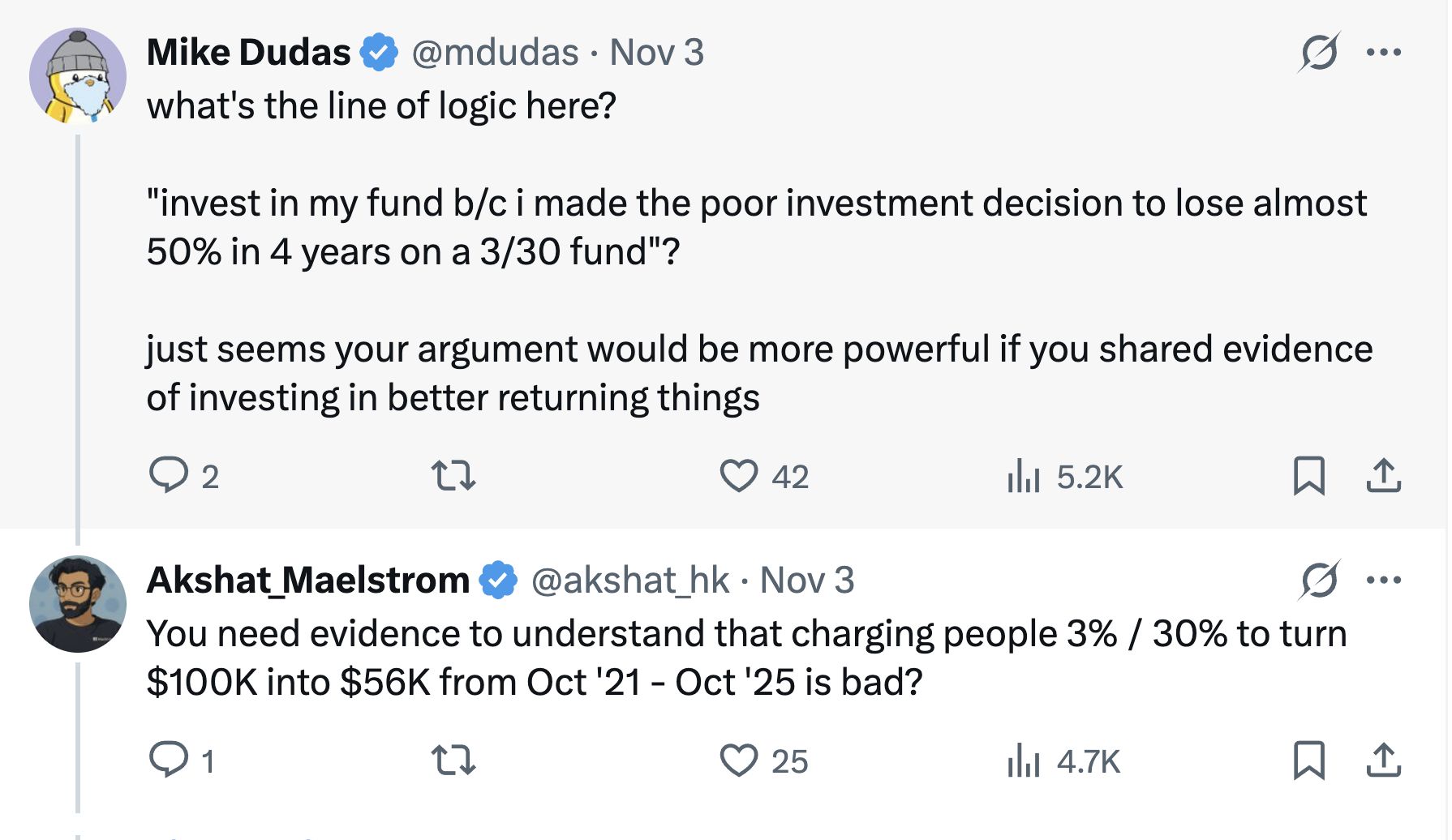

It is worth mentioning that in this controversy, some comments believe that Vaidya’s public criticism of his peers is somewhat “marketing-oriented”—as the head of Arthur Hayes’ family office, he is also formulating differentiated strategies and raising funds for his own fund—Maelstrom is preparing a new fund of over $250 million, planning to acquire mid-sized crypto infrastructure and data companies.

Therefore, Vaidya may be using criticism of competitors to highlight Maelstrom’s differentiated positioning focused on value investing and cash flow. Mike Dudas, co-founder of 6th Man Ventures, commented that if he wants to promote the performance of his family office’s new fund, he should let his own results speak, rather than attract attention by attacking others.

“No Strategy Beats Buying BTC”

Vaidya used his own experience to compare fund returns with a simple bitcoin holding strategy, raising an age-old question: For investors, is it better to give money to a crypto fund, or just buy bitcoin directly?

The answer to this question may vary at different times.

In earlier bull cycles, some top crypto funds significantly outperformed bitcoin. For example, during the market frenzies of 2017 and 2020–2021, sharp fund managers achieved returns far exceeding bitcoin by getting in early on emerging projects or using leverage strategies.

Outstanding funds can also provide professional risk management and downside protection: in bear markets, when bitcoin prices are halved or fall even further, some hedge funds have successfully avoided huge losses or even achieved positive returns through shorting and quantitative hedging strategies, thus relatively reducing volatility risk.

Secondly, for many institutions and high-net-worth investors, crypto funds offer diversified exposure and professional access. Funds can invest in areas that individual investors can hardly access, such as private token rounds, early-stage equity, and DeFi yields. The seed projects Vaidya mentioned that soared 20–75 times are difficult for individuals to access at early valuations without the channels and professional judgment of funds—provided that fund managers truly have outstanding project selection and execution capabilities.

From a long-term perspective, the crypto market changes rapidly, and professional investing and passive holding each have their own suitable scenarios.

For practitioners and investors in the crypto space, the controversy surrounding the Pantera fund offers an opportunity—to rationally evaluate and choose investment methods that suit their own strategies in the ever-changing crypto market, in order to maximize wealth growth.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The myth of a 100% win rate shattered: Why did the whales sink in this tsunami?

Wall Street’s Calculation: What Does $500 Million Buy in Ripple?

Swipe to place bets? How Warden is disrupting prediction markets with the Tinder model

Dalio warns: A new round of quantitative easing is pushing the market to the brink of a bubble